You've got a retirement calculator, a 401(k) balance you're proud of, and a vague sense that you're "on track." So why does it feel like you're navigating a minefield blindfolded? Here's the ugly truth: most people don't fail at retirement because they saved too little. They fail because they never sat down and forced themselves to answer the hard questions on paper. That's exactly why retirement planning worksheets aren't just helpful—they're the difference between crossing your fingers and actually knowing where you stand.

Look, honestly, I've been writing about personal finance for over a decade, and the number one thing I see is people treating retirement like a math problem when it's really a behavior problem. You can't optimize your way out of a future you've never visualized. Right now, inflation is eating away at purchasing power, market volatility is making your "safe" assumptions look shaky, and the old rules about 4% withdrawal rates feel like they were written for a different planet. You need something concrete to hold onto. Something that forces you to confront the gap between your dreams and your spreadsheets.

Here's what I'm not going to do—I'm not going to hand you a generic checklist that makes you feel productive for ten minutes. The worksheets I'm talking about are the kind that make you uncomfortable. They ask about your worst-case healthcare scenario, your actual spending habits (not the ones you brag about at dinner parties), and what happens if you live to 95. That's the point. By the time you finish this guide, you'll have a document that feels less like a homework assignment and more like a personal map. One that actually accounts for the fact that you might want to travel more or, I don't know, buy a boat you'll probably regret. The math is the easy part. The honesty? That's the work.

Let's be honest: most retirement advice reads like it was written by a robot that's never had to decide between funding a Roth IRA or fixing a leaky roof. You get the big picture—save more, spend less, invest wisely—but the rubber never meets the road. That's where the real friction lives. The gap between knowing what to do and actually doing it is where most people's retirement dreams quietly die. And that gap is exactly where a good set of structured planning tools can pull you back from the edge.

Why Your Spreadsheet Probably Lied to You (and What Actually Works)

I've seen people spend weeks building elaborate spreadsheets with color-coded cells and complex macros. They look impressive. They're almost always wrong. The problem isn't the math—it's the assumptions. People plug in a 7% annual return, forget about inflation, and assume their spending habits won't change for thirty years. That's fantasy, not planning. What actually works is a system that forces you to confront your specific numbers, not generic averages. Your biggest risk isn't market volatility; it's your own unexamined spending patterns.

Here's what nobody tells you: the most valuable part of any planning exercise isn't the final number. It's the moment you realize your projected expenses are 15% higher than you estimated because you forgot to account for replacing a car every eight years. That gut-check is worth more than any theoretical portfolio projection. And yes, that actually matters more than chasing the perfect asset allocation. A solid framework will make you uncomfortable—that's the point. If you breeze through it, you're probably lying to yourself.

What a Realistic Plan Actually Forces You to Confront

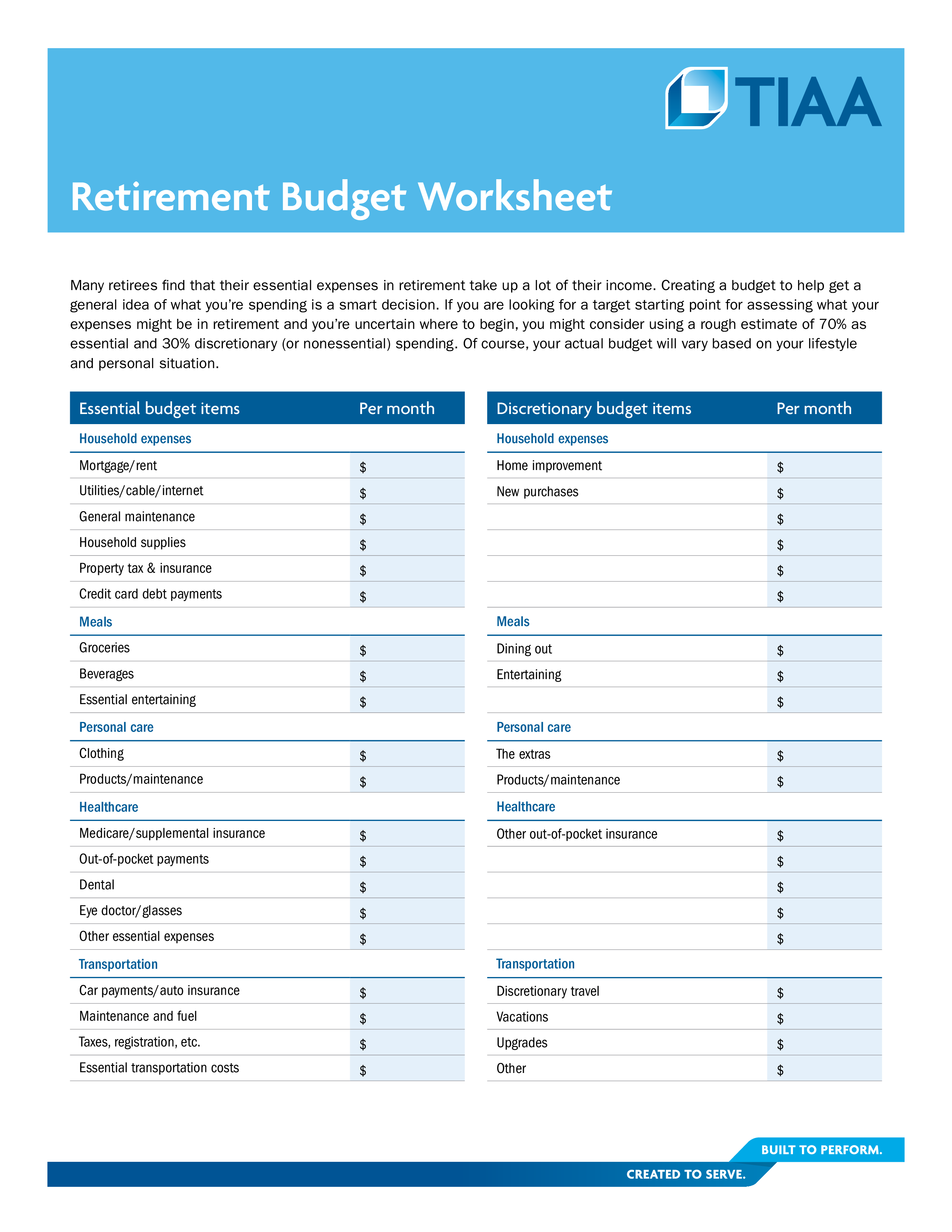

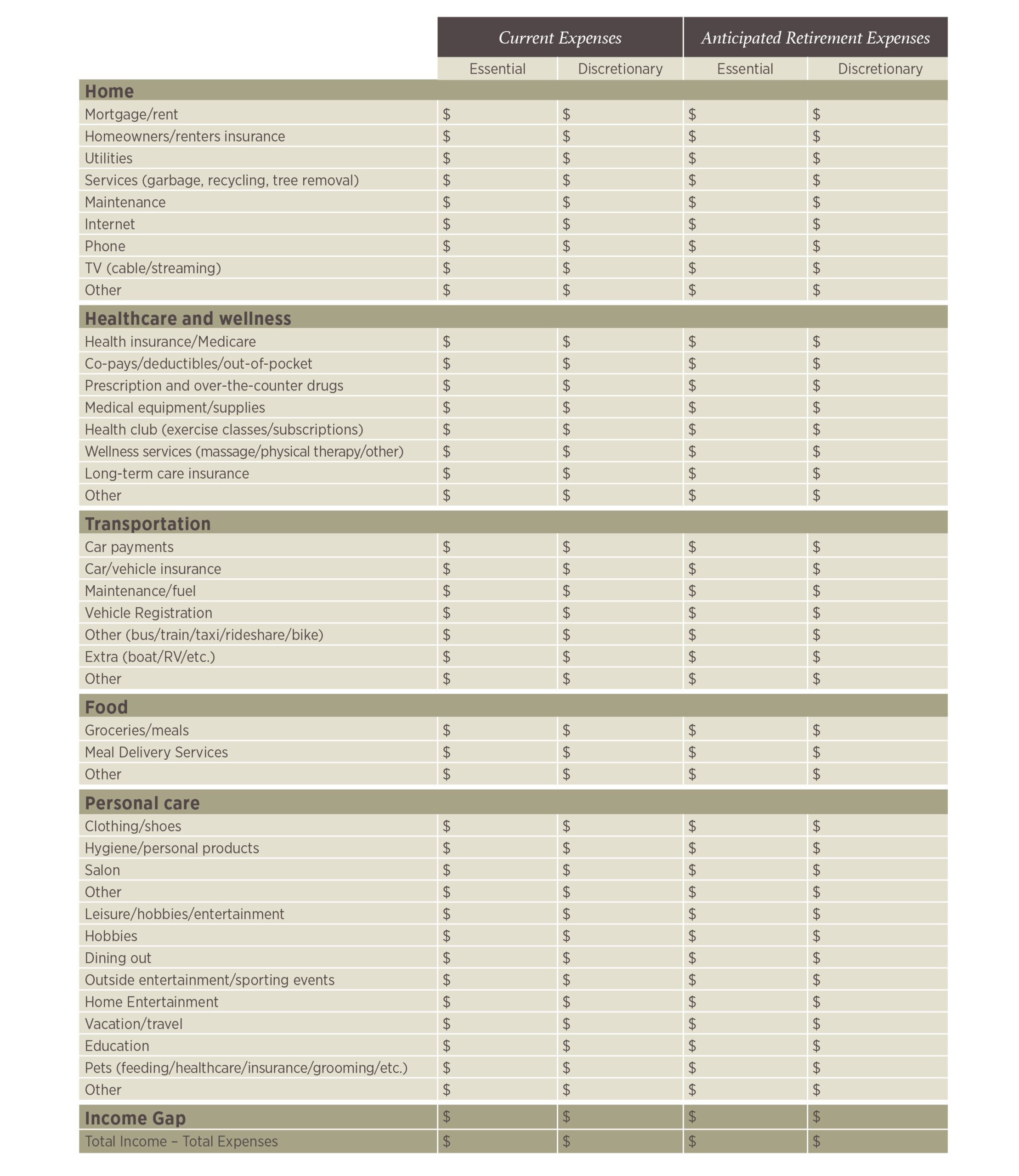

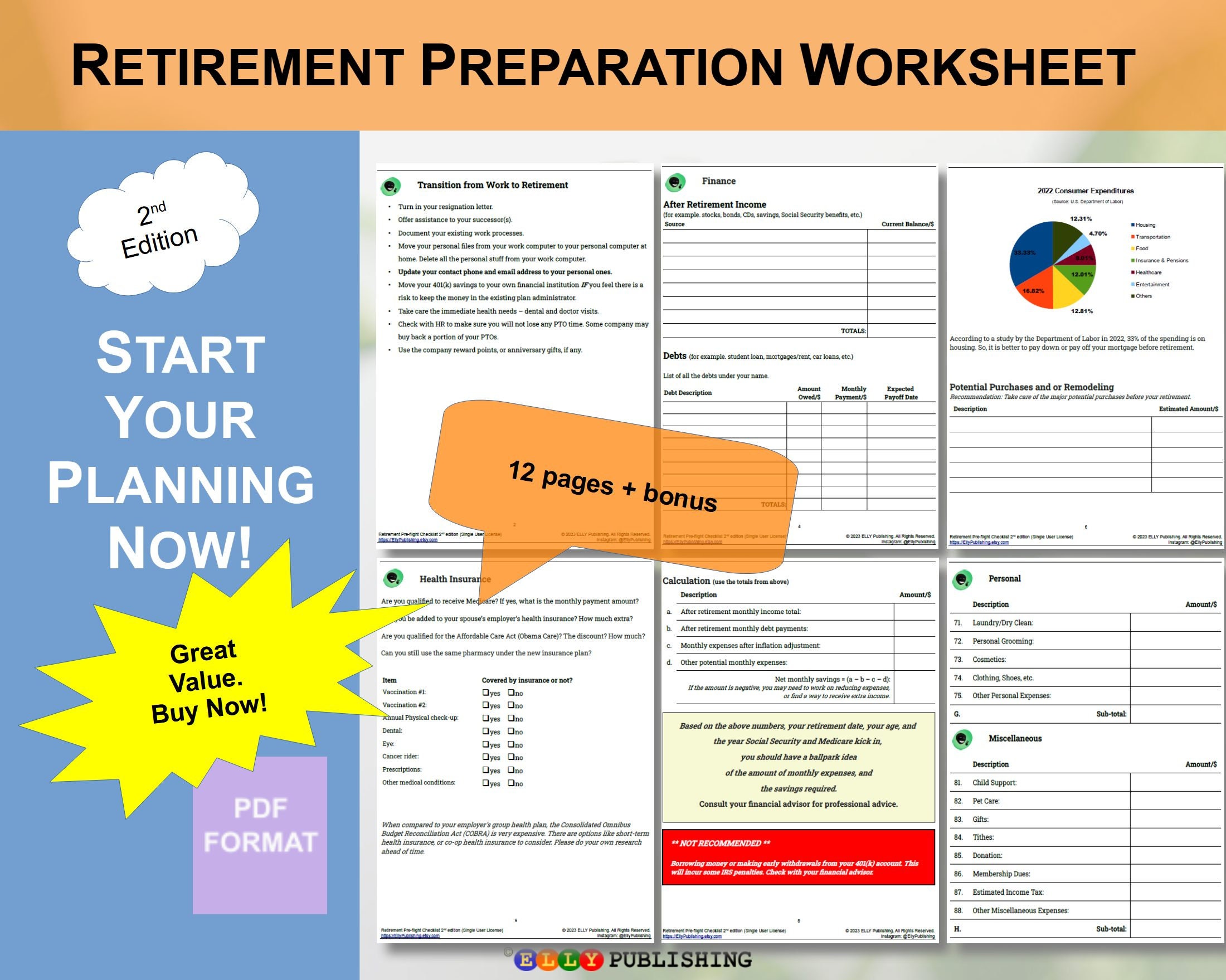

Most people skip the boring stuff: healthcare costs in your 70s, home maintenance in your 80s, and the very real possibility that you'll live longer than your money. A good worksheet doesn't just ask for your current income. It makes you estimate your annual spending in retirement by category—housing, food, travel, medical, and the inevitable "miscellaneous" that always eats your budget. The single most actionable tip I can give you: take your current monthly spending, subtract what you won't need in retirement (commuting costs, work clothes, 401k contributions), and then add 20% for healthcare and fun. That's your real number. Most people find it's higher than they expected.

Where Most People Get Tripped Up (and How to Avoid It)

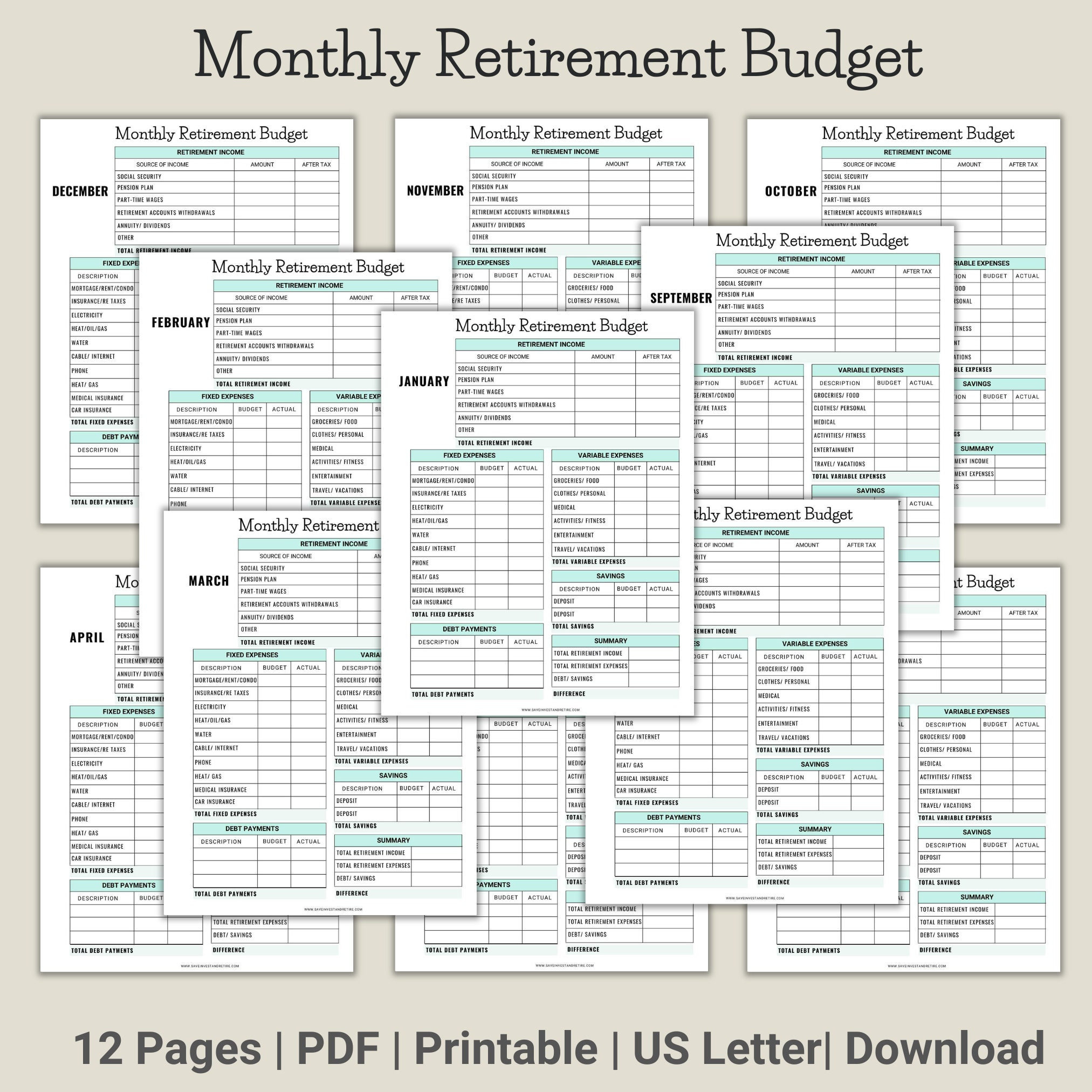

The common mistake is treating this like a one-and-done exercise. You fill it out, feel a brief sense of control, and then file it away until next year. That's like checking your blood pressure once and assuming you're fine forever. Your income changes. Your health changes. The market does its thing. A living document—one you revisit every six months—is worth ten times a static plan. I recommend setting a recurring calendar reminder for the first week of April and October. Spend thirty minutes updating your numbers. That small habit will save you from the shock of discovering at 62 that you're short by six figures.

A Simple Way to Compare Your Options Without the Overwhelm

When you're looking at different approaches to structuring your retirement income, the options can feel paralyzing. Here's a straightforward comparison of three common strategies. They're not mutually exclusive, but most people lean heavily toward one.

| Strategy | Best For | Key Risk | Typical Annual Effort |

|---|---|---|---|

| Total Return (4% Rule) | Investors comfortable with market swings | Sequence-of-returns risk early in retirement | 2-3 hours rebalancing |

| Income Floor (Annuities + Pensions) | People who hate volatility | Inflation erosion and fees | 1 hour reviewing statements |

| Bucket Strategy (Cash + Bonds + Stocks) | Those who want structure without complexity | Behavioral discipline during bear markets | 4-6 hours annual rebalancing |

The bucket strategy often wins for people who want the emotional safety of cash reserves without giving up growth potential. But none of these work without the foundational work of knowing your actual numbers first. A structured planning document isn't a magic wand—it's a mirror. And sometimes the reflection is uncomfortable. But uncomfortable is better than surprised, and surprised is better than broke.

The Part Most People Skip

You’ve spent the last several minutes digging into the mechanics of building a secure future—calculating expenses, projecting income, and mapping out timelines. That’s the hard work, and you should feel good about it. But here’s the truth that separates a plan that collects dust from a plan that actually works: the moment you close this tab, the real test begins. Will you take the next step, or will life’s daily noise sweep this clarity away? This isn’t about perfection; it’s about momentum. A single afternoon of focused effort can set a financial foundation that carries you through decades of change, peace of mind, and unexpected opportunities. That’s why this topic matters beyond numbers—it’s about giving yourself permission to prioritize your own future.

Maybe you’re thinking, “I’ll come back to this when I have more time,” or “I’m not sure I have all my data ready yet.” That doubt is normal—it’s the same voice that keeps people stuck in indecision for years. But here’s the warm truth: you don’t need every number perfect. You don’t need a flawless spreadsheet. What you need is a starting point, and you already have it. The retirement planning worksheets you’ve seen here are tools, not tests. They’re designed to meet you exactly where you are, whether you’re a spreadsheet pro or someone who avoids math like a Monday morning. Give yourself grace, but give yourself action.

So here’s your soft invitation: bookmark this page right now. Save it to a folder you’ll actually open later. Or better yet, forward it to one person who could use a nudge—a partner, a friend, a sibling who keeps saying “I’ll start next year.” Because when you share what you’ve learned, it becomes real. And if you want to explore more practical resources, take a moment to browse the gallery of retirement planning worksheets available here—they’re waiting to turn your intentions into a plan that actually sticks. The best time to start was yesterday. The second best time is right now.