Most people spend more time planning a two-week vacation than they do planning thirty years of retirement. Honestly, that terrifies me — and it should terrify you too. Because without a real system, you're just guessing. That's exactly why I want you to grab a retirement planning worksheet pdf before you read another word. Not because worksheets are fun (they're not), but because this one forces you to stop pretending and start calculating.

Look — you're probably reading this because you've got that nagging feeling. The one that whispers you're behind. Or maybe you're ahead but have no clue if that's actually true. Right now, inflation is eating savings alive, and retirement ages keep creeping upward. The old rules don't apply anymore. What worked for your parents? It's not going to cut it for you. That's not pessimism — it's just math.

Here's what I want you to understand: this worksheet isn't about some theoretical "ideal retirement." It's about the numbers that actually matter to your life. How much you need to cover your bills. When you can realistically stop working. Whether that cabin in the mountains is a dream or a delusion. I've seen people cry with relief after filling it out — because suddenly the fog clears. You'll get that too. But only if you stop scrolling and start writing.

Let's be honest for a second: most retirement planning advice reads like it was written by a robot that has never actually worried about money. You get generic percentages, vague timelines, and a lot of "save more" without any real structure. That's exactly why a retirement planning worksheet pdf isn't just a nice-to-have—it's the difference between guessing your future and actually building it. I've seen too many people skip the worksheet step and end up five years from retirement with nothing but Social Security and hope.

The Part of Retirement Planning Most People Get Wrong

Here's what nobody tells you: the hardest part isn't the math. It's the assumptions. Most worksheets ask you to guess your retirement expenses, your rate of return, and your life expectancy. Those are three massive unknowns. A good retirement planning worksheet pdf forces you to confront those numbers honestly, not optimistically. And yes, that actually matters because if you're off by just 2% on your assumed annual return, you could be short by six figures over thirty years.

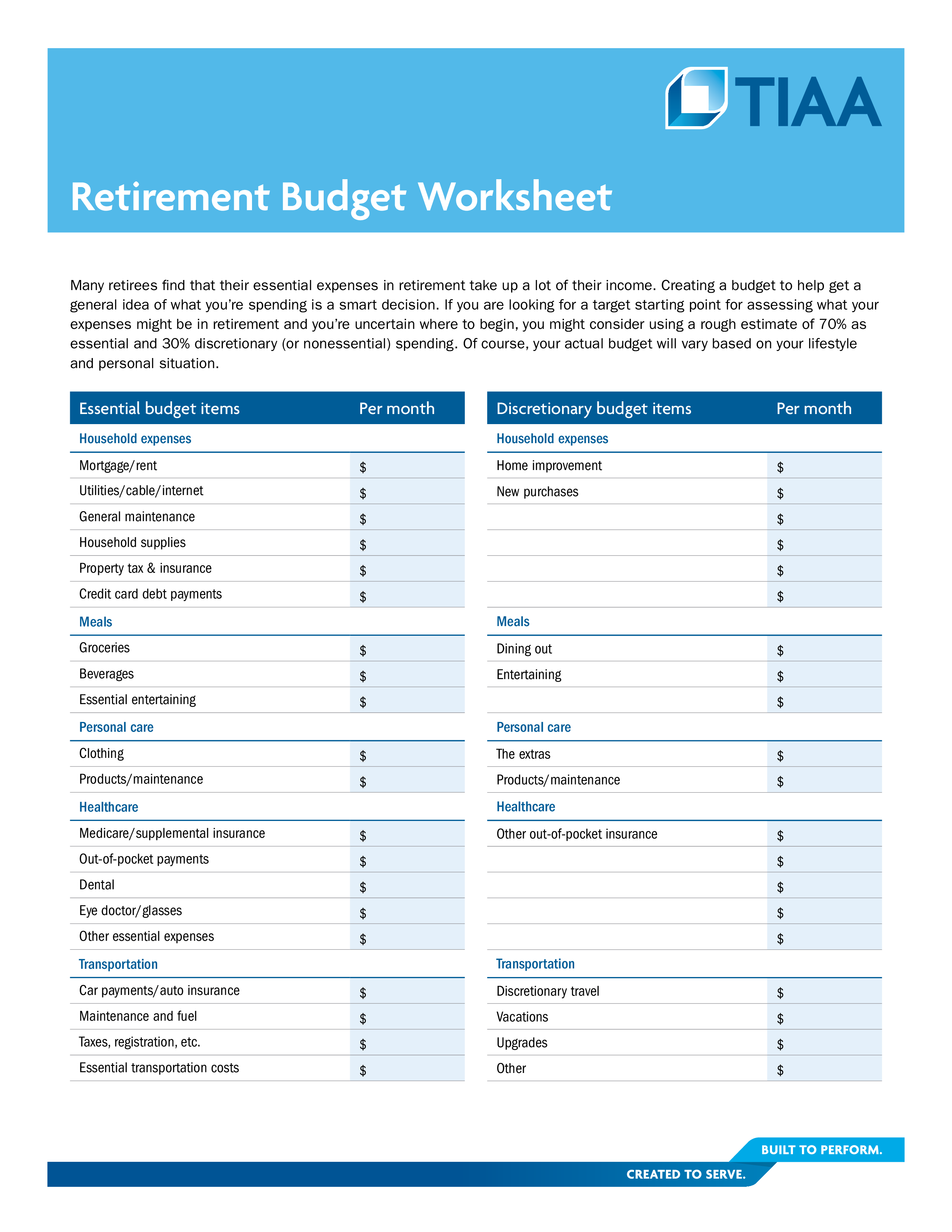

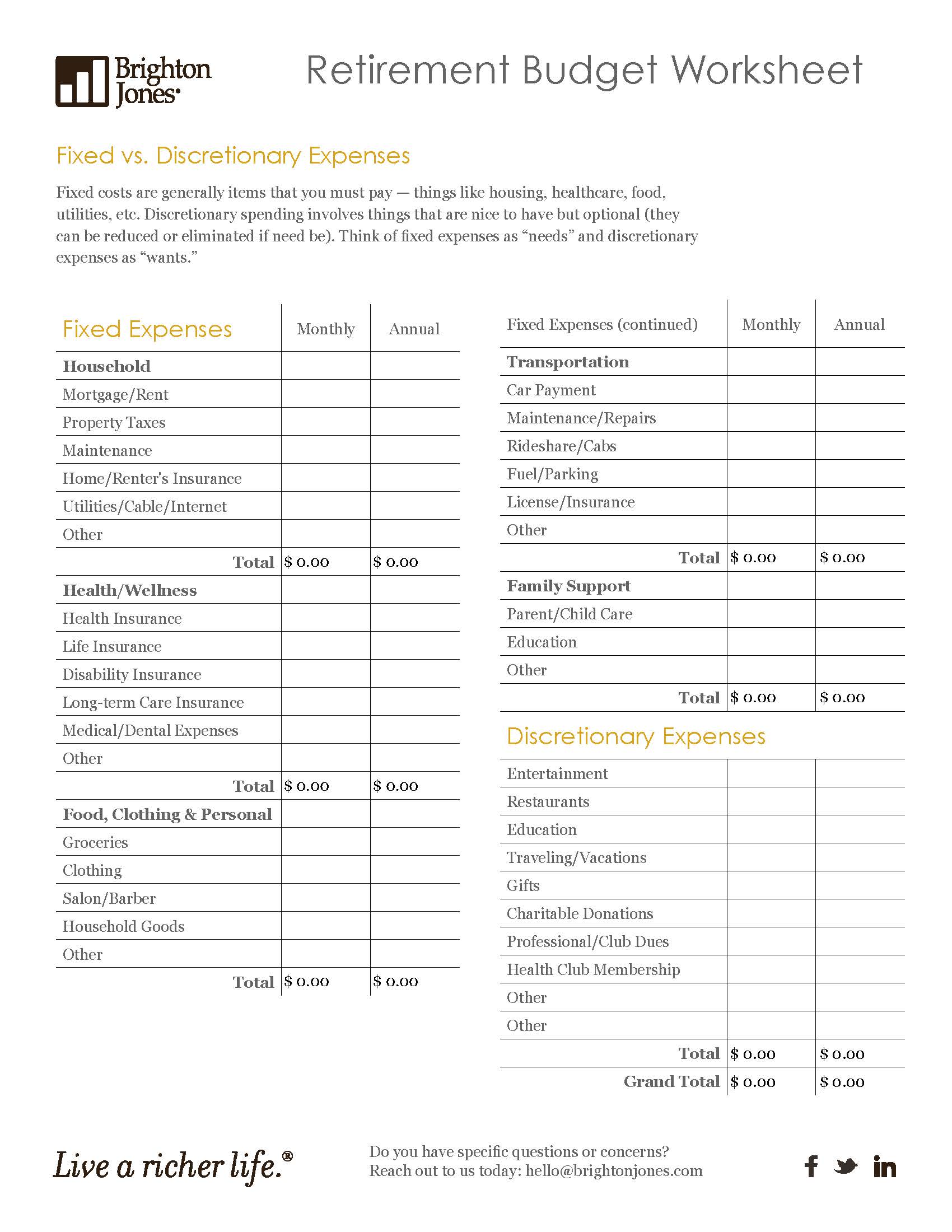

I've worked with dozens of planners, and the ones who actually help their clients are the ones who use worksheets that break down expenses into fixed, variable, and discretionary buckets. Not just "you'll need 80% of your current income." That rule is lazy. A proper worksheet makes you list your actual spending categories—groceries, healthcare, travel, home maintenance—and then apply realistic inflation rates to each one. Healthcare inflation runs about 5-6% annually, not the 2-3% you see on generic calculators. That single adjustment can change your entire savings target.

Why a Static Worksheet Fails Most People

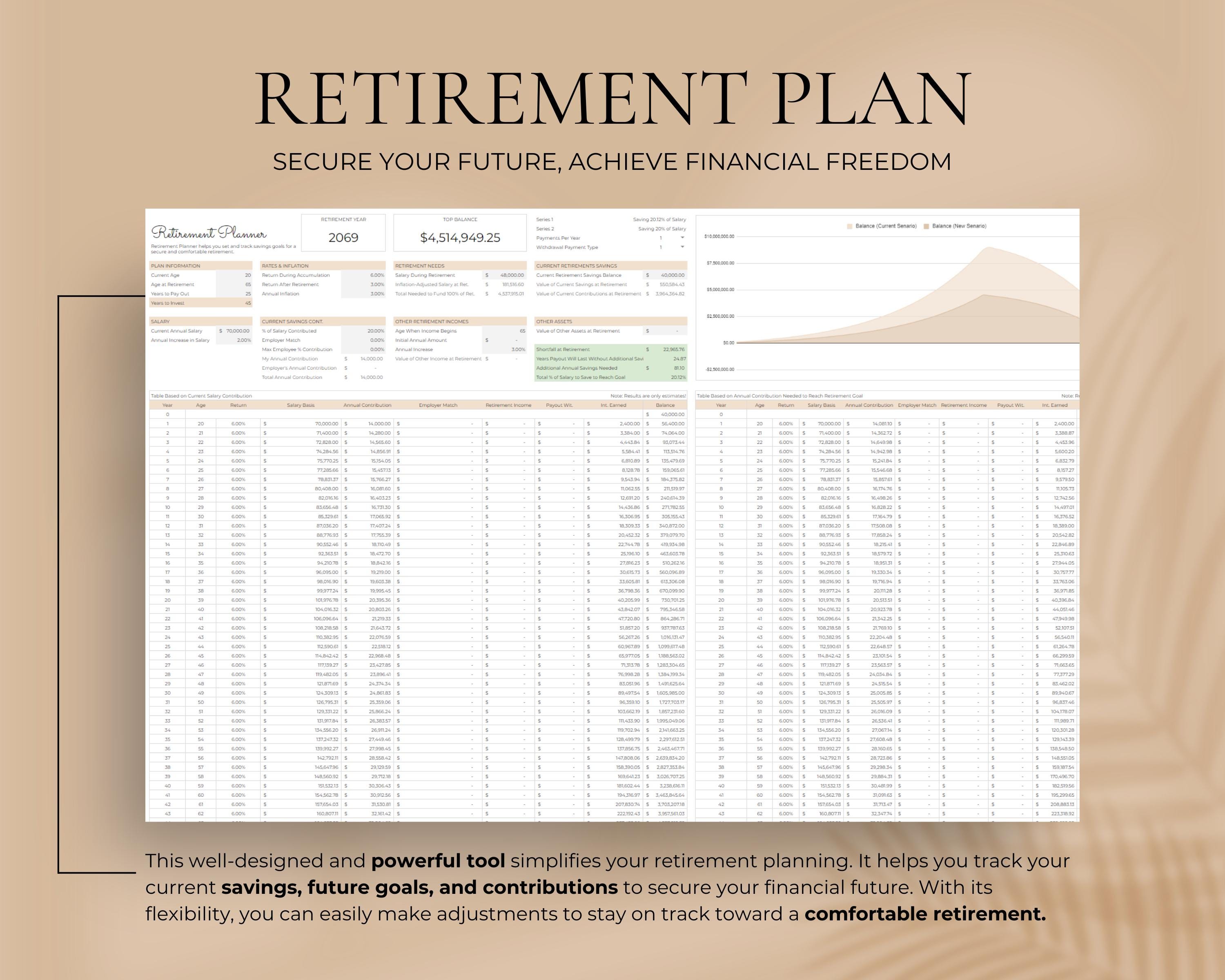

Most downloadable worksheets are static. You fill it out once, file it away, and forget it. That's a mistake. Your retirement plan needs to be a living document. The best approach is to revisit your retirement planning worksheet pdf every twelve months and adjust for real-world changes—a promotion, a market downturn, a new health diagnosis. I recommend keeping three versions: your current plan, a "worst case" scenario where returns are flat for a decade, and a "best case" where you might retire early. That range gives you clarity without panic.

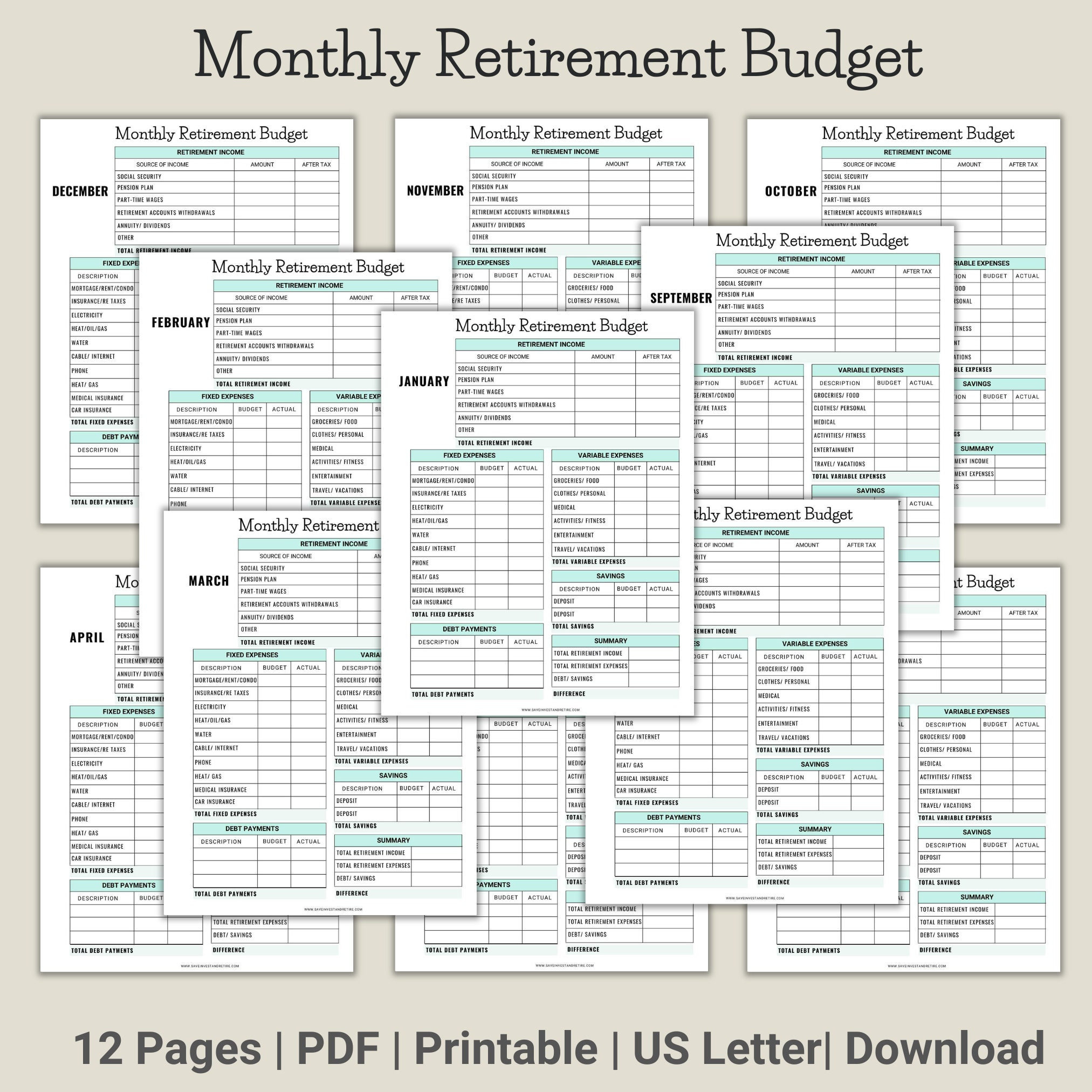

Real Numbers: What a Good Worksheet Should Track

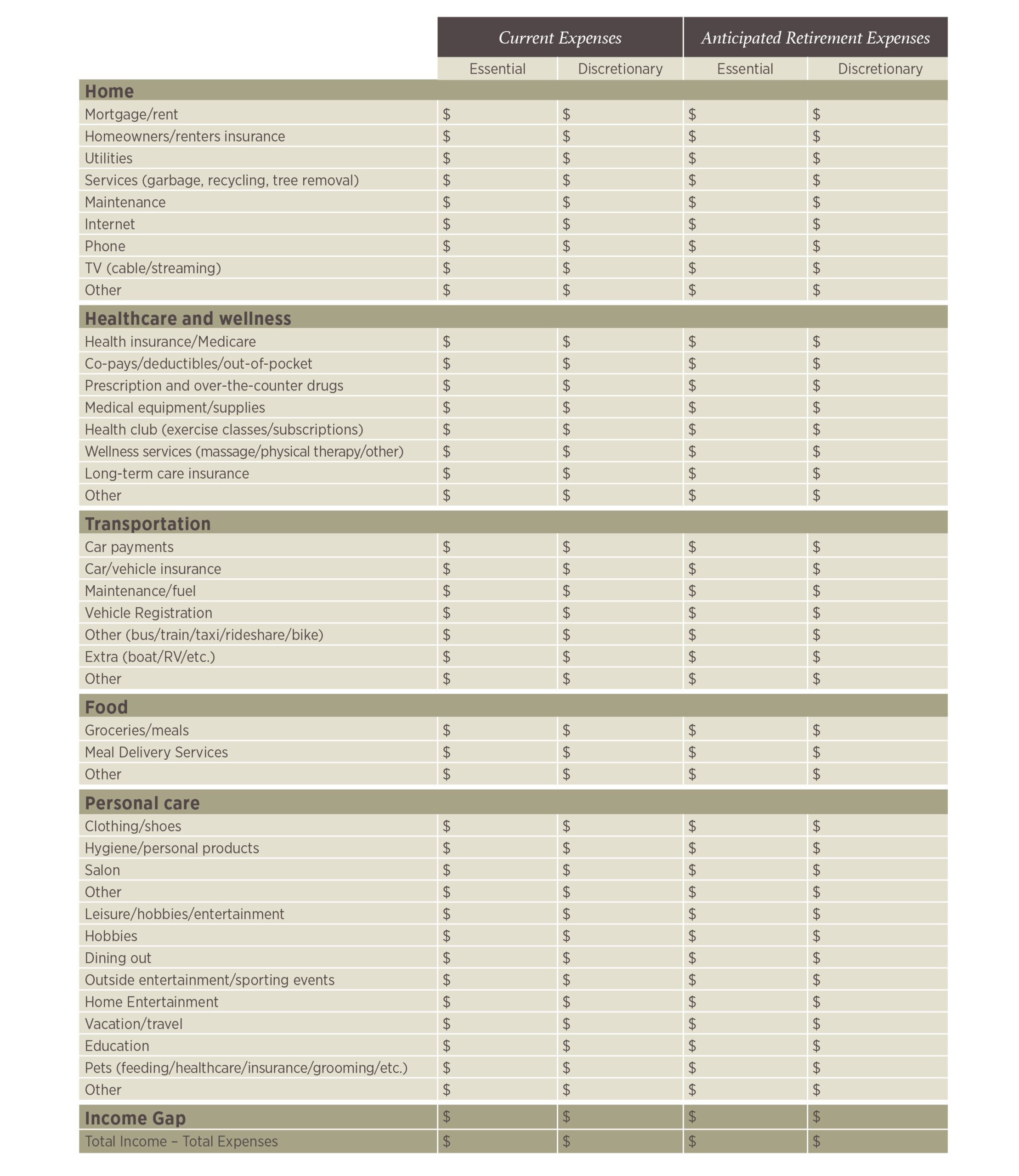

If your worksheet only asks for your 401(k) balance and your expected Social Security benefit, it's too shallow. A useful spreadsheet tracks at least five income sources and seven expense categories. Here's a simple breakdown of what a solid worksheet should capture:

| Income Source | Typical Annual Amount | Growth Assumption |

|---|---|---|

| Social Security (age 67) | $24,000 - $36,000 | 2.5% COLA |

| Pension (if applicable) | $12,000 - $30,000 | Fixed or 1% COLA |

| 401(k) / IRA withdrawals | 4% of balance annually | 6-8% portfolio return |

| Part-time work | $10,000 - $20,000 | None (assume flat) |

| Rental income | $6,000 - $18,000 | 3% annual rent increase |

Notice how the assumptions vary? That's the point. A cookie-cutter retirement planning worksheet pdf that uses one growth rate for everything is misleading. You need to separate guaranteed income from market-dependent income. Social Security and pensions are your floor. Your investment withdrawals are your upside—and your risk.

The One Actionable Tip That Changes Everything

Here's the specific move that most people skip: stress-test your worksheet with a 15-year bear market scenario. Run the numbers assuming zero real returns for the first fifteen years of retirement. If your portfolio still survives until age 90, you're in good shape. If it fails, you need to adjust your withdrawal rate or your spending. I did this for a client last year who thought he was fine. Turned out his plan ran out of money at age 82 under a conservative scenario. We cut his projected travel budget by 15% and added a part-time consulting gig. That single worksheet revision bought him ten more years of security. Don't skip this step. A good retirement planning worksheet pdf should have a "stress test" tab or column built in. If yours doesn't, add one yourself. It's the most honest conversation you'll ever have with your money.

One Last Thing Before You Go

Here’s the truth about financial freedom: it’s not built in a single dramatic moment. It’s built in the quiet afternoons when you choose clarity over confusion. Every number you track, every goal you write down, every honest look at where your money is going — that’s the real work. That’s what turns a vague hope into a concrete path. This matters because your future self isn’t some distant stranger; they’re you in a few decades, waking up to the choices you made today.

Maybe you’re thinking, “I’ll get to it later,” or “This feels too complicated.” I get it. Most people feel that way — and that’s exactly why most people stay stuck. But you’re not most people. You’re here, reading this, which means you already have the desire. All you need is a starting point. And you have it: the retirement planning worksheet pdf is your anchor, not a puzzle. One page at a time, one box filled in. That’s all it takes.

So here’s your next step: bookmark this page right now. Open that retirement planning worksheet pdf and leave it on your desktop. Share the link with a friend who’s been putting this off — you’ll be the one who finally nudged them forward. Browse the gallery of tools we’ve gathered here. Don’t overthink it. Just start. Your future self is already grateful.