Most people spend more time planning their next vacation than their retirement. That's a problem — and it's exactly why a simple retirement planning worksheet excel can save you from waking up at 65 wondering where all your money went.

Here's the thing: you probably think you have time. Maybe you do. But the math on retirement isn't forgiving, and the calculators banks give you are either too vague or designed to sell you something. Real talk — I've seen friends in their 50s panic because they assumed their 401(k) would just "work out." It doesn't work out unless you track it. Right now, inflation is eating savings alive, and the old rules about saving 10% of your income? Laughable. You need a system that's yours, not a generic retirement quiz from a website. Honestly, a spreadsheet you build yourself is the only way to stop guessing and start knowing.

What I'm going to show you isn't just a template — it's a way to see your future in black and white. No fluff. No motivational nonsense about lattes. You'll get a worksheet that actually accounts for the messy stuff: irregular income, surprise expenses, and that nagging feeling you're behind. By the time you finish reading, you'll know exactly which numbers matter and how to bend them in your favor. Stick with me — this is the boring stuff that actually changes your life.

Let's be honest for a second: most retirement planning advice feels like it was written by a robot for a robot. You get vague suggestions about saving "enough" and "starting early," but nobody hands you the actual tool to run the numbers. That's where a decent spreadsheet comes in. But here's what nobody tells you—the real value of a retirement planning worksheet Excel isn't the formulas. It's the brutal honesty it forces on your assumptions. You can't hide from a cell that calculates your shortfall in red.

The Part of Financial Modeling Most People Get Wrong

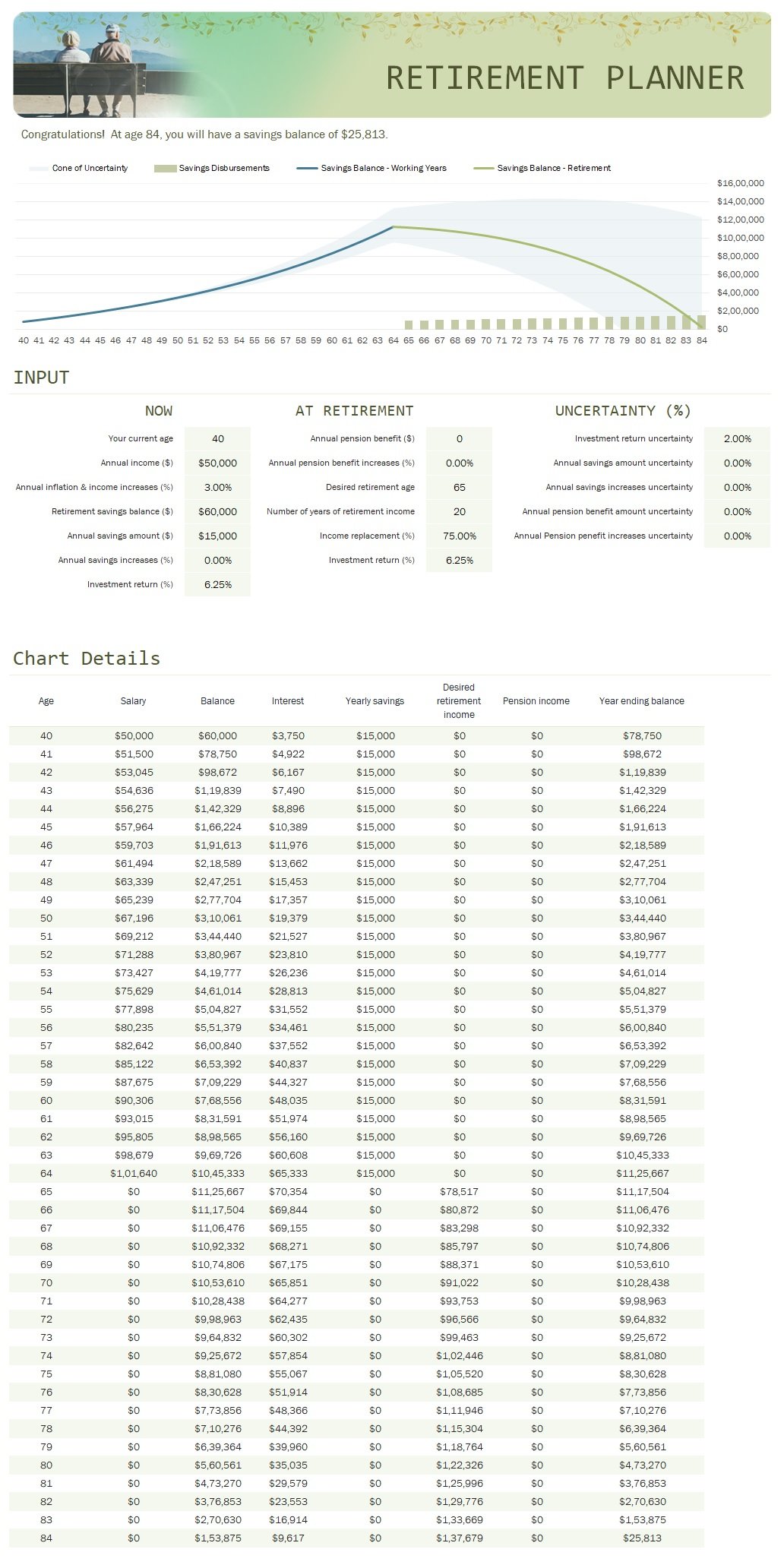

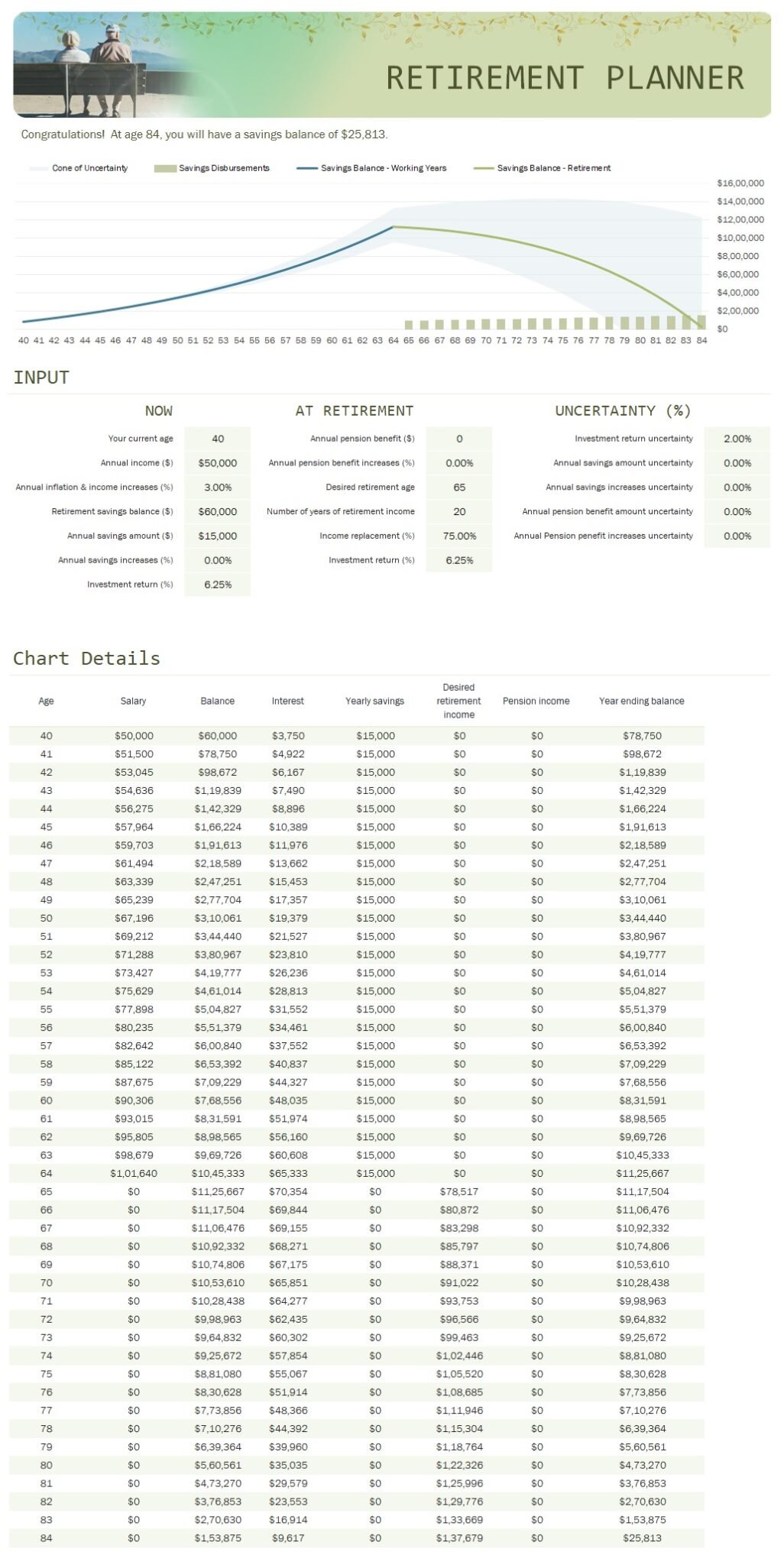

Most folks treat their retirement spreadsheet like a dream board. They plug in an 8% annual return, assume 3% inflation, and call it a day. That's not planning—that's wishful thinking. The true power of a well-built retirement calculator lies in stress-testing your worst-case scenarios. What happens if the market tanks 30% in your first year of retirement? What if you live to 95 instead of 85? A rigid spreadsheet built on static numbers will lie to you. You need a model that lets you toggle variables like Social Security claiming age, part-time work income, and sequence-of-returns risk. And yes, that actually matters more than your rate of return. I've seen people with modest savings retire comfortably simply because they modeled a conservative 4% withdrawal rate and stuck to it. Meanwhile, high earners with flashy portfolios crashed because they never simulated a bear market in year one.

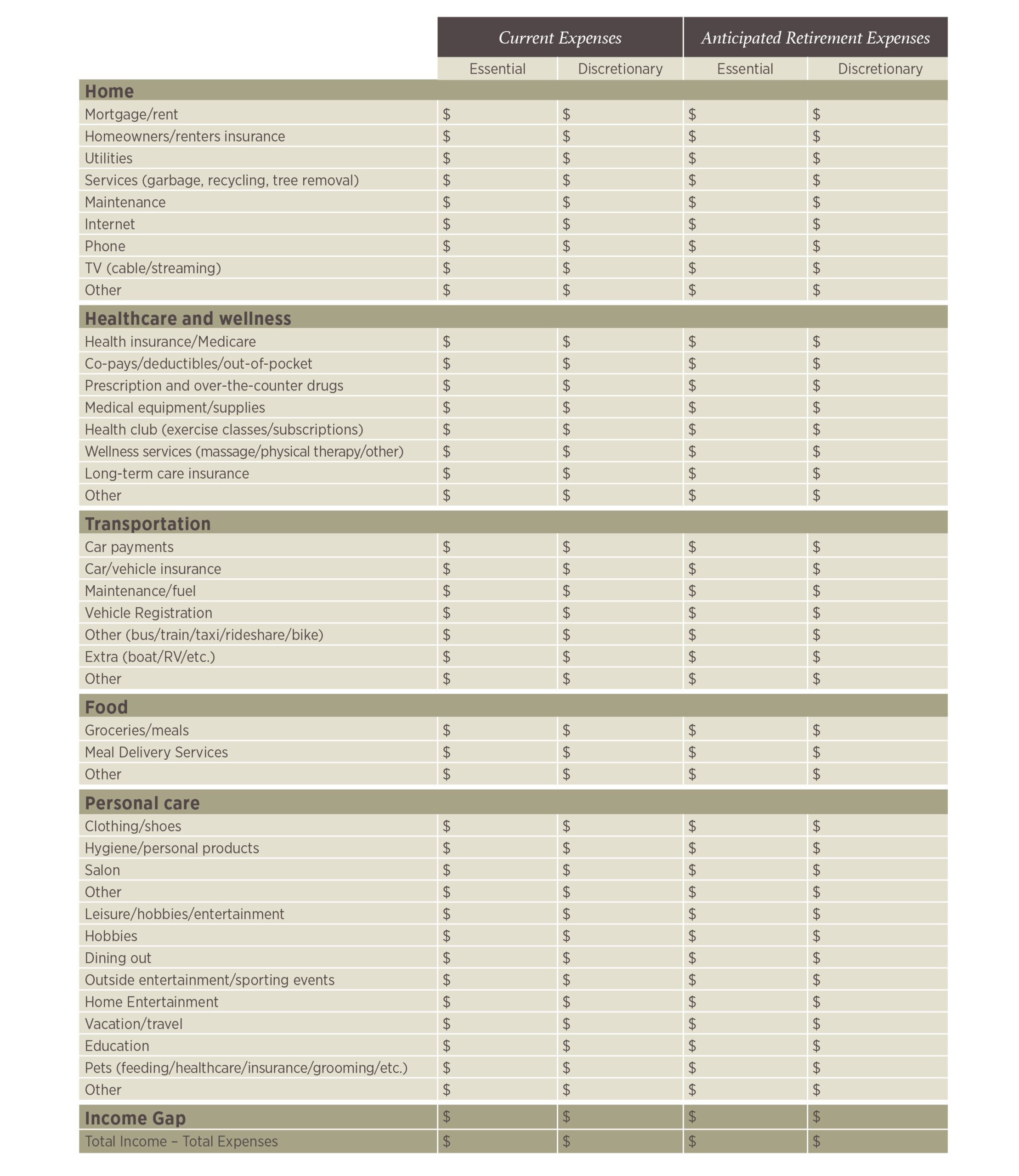

What Your Spreadsheet Must Include to Be Useful

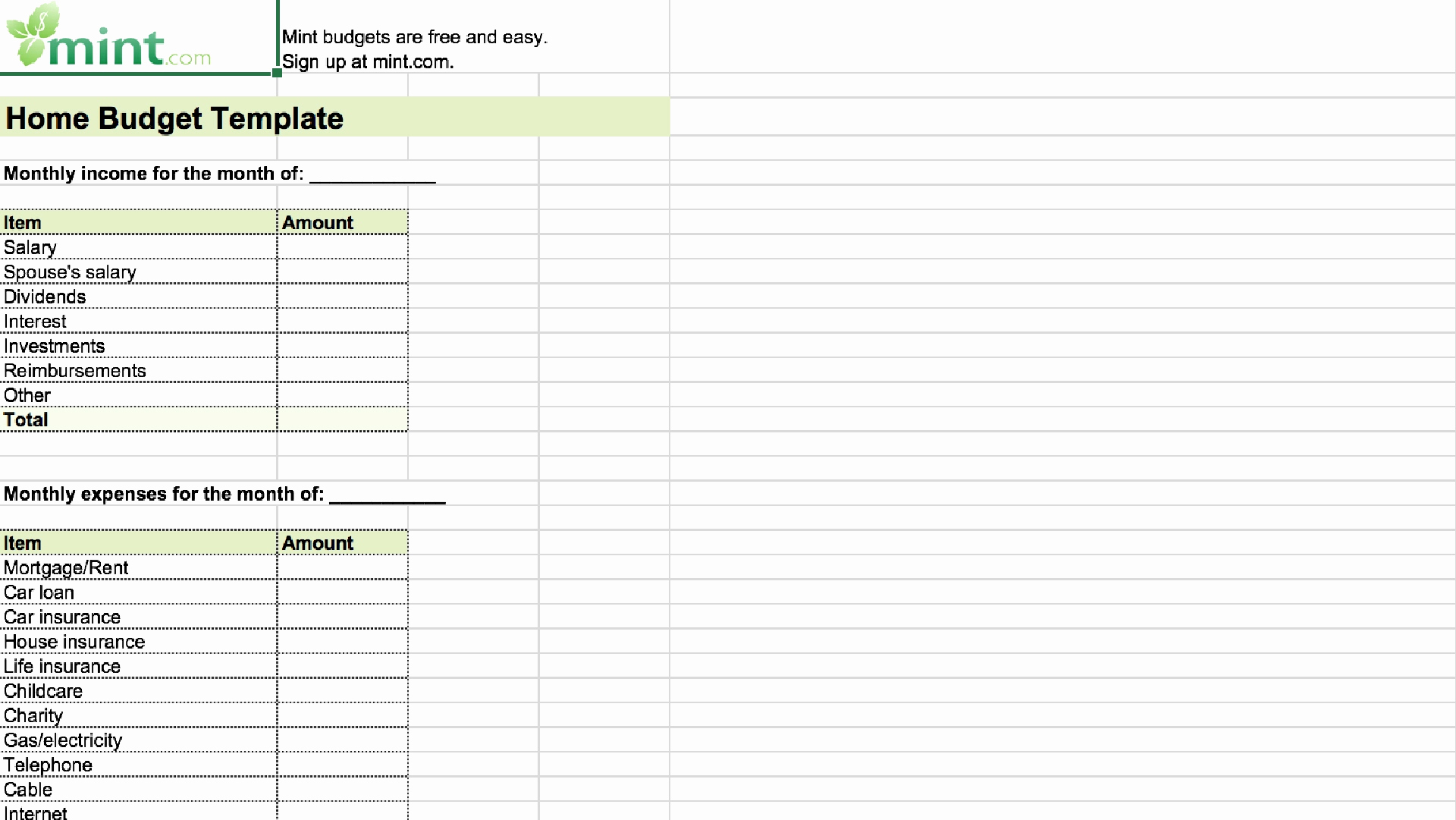

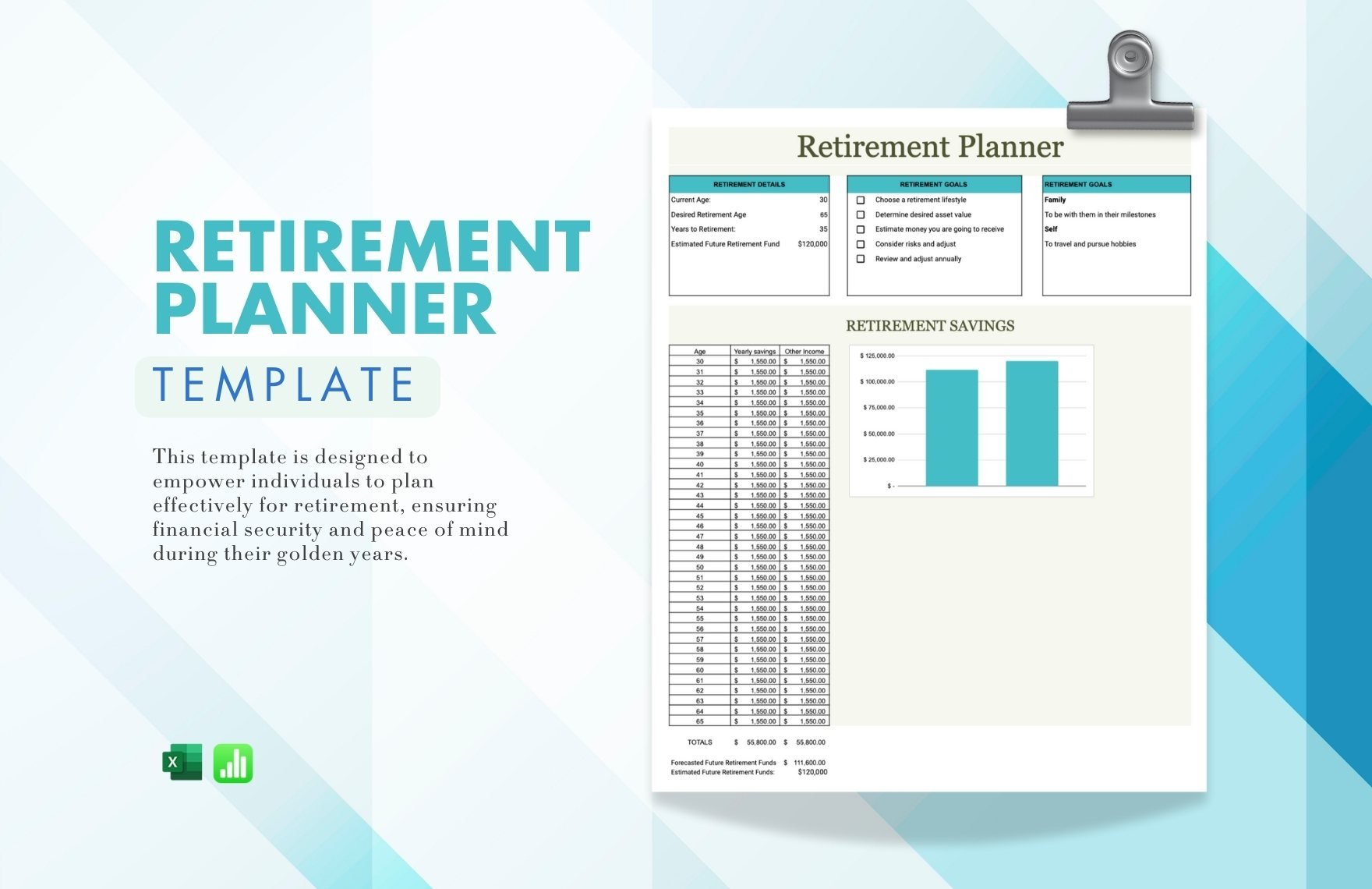

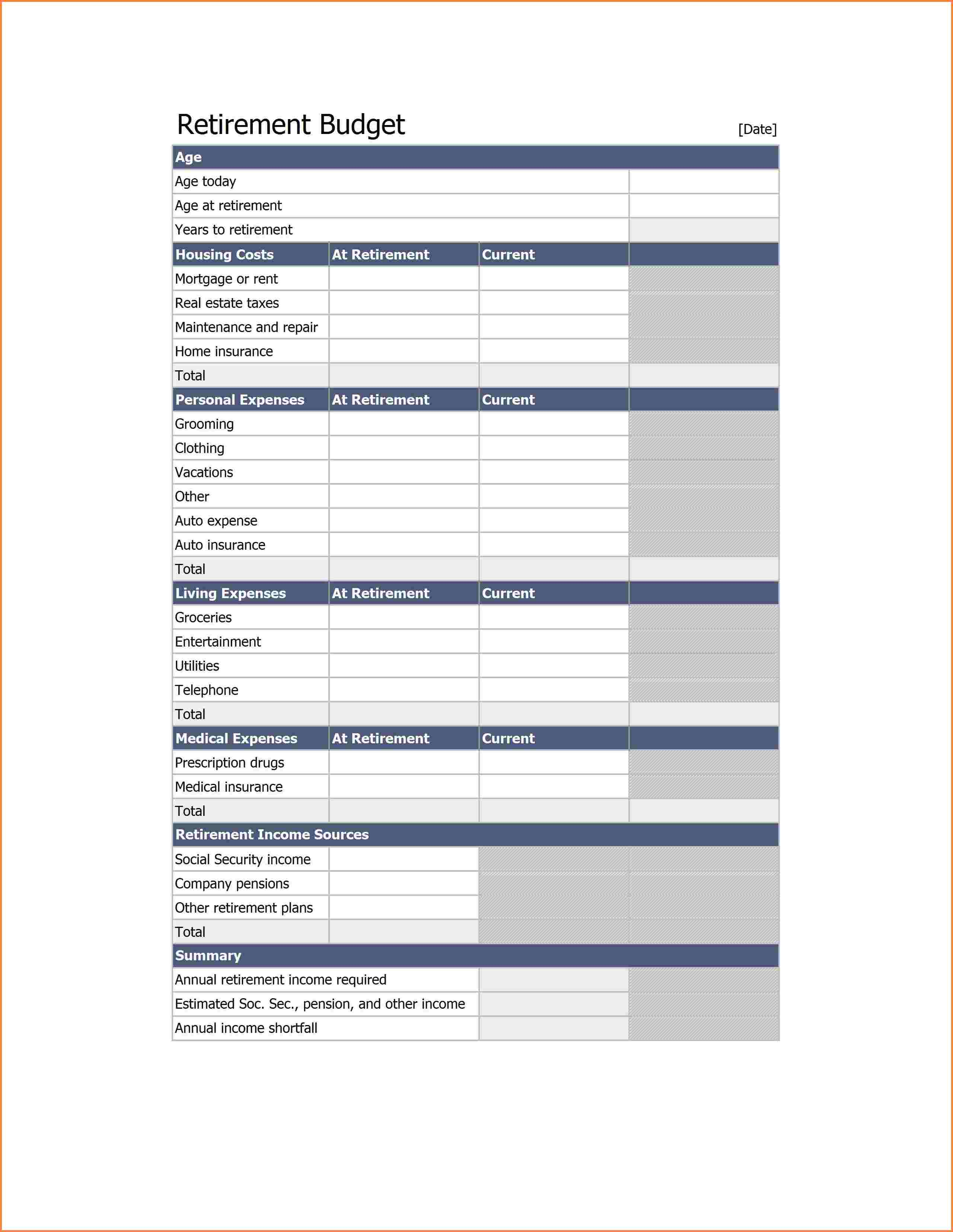

If your worksheet only tracks your 401(k) balance and a vague "other savings" line, you're missing half the picture. A proper retirement planning worksheet Excel needs to account for lumpy expenses—the new roof, the wedding gift, the year you decide to travel Europe for three months. Your biggest risk isn't inflation; it's underestimating one-time costs. Build a dedicated row for irregular spending. Also, separate your accounts by tax treatment: pre-tax (traditional 401k/IRA), Roth (tax-free growth), and taxable brokerage. Why? Because how you withdraw matters almost as much as how much you save. A tax-ignorant withdrawal strategy can cost you six figures over thirty years. Your spreadsheet should have a column for estimated tax drag on each account type.

How to Actually Use the Tool (Not Just Build It)

Here's the actionable tip that changes everything: once you have your worksheet built, run three scenarios every January. Scenario A: optimistic (5% returns, low inflation). Scenario B: moderate (4% returns, normal inflation). Scenario C: pessimistic (2% returns, high inflation). Only plan your spending based on Scenario C. If you can make that work, everything else is gravy. I once worked with a client who had a million-dollar portfolio but was terrified to retire. We ran the pessimistic model—he still had money at age 92. He retired the next month. That's the kind of clarity a spreadsheet gives you. It removes the emotional noise. Most people stop using their worksheet after they build it. Don't be that person. Revisit it quarterly. Treat it like a living document, not a trophy.

Why Most Templates Fail (and How to Fix Yours)

The free templates you find online are dangerous. They're generic, they ignore Social Security timing nuances, and they almost never account for healthcare inflation—which runs at double the general rate. A good retirement planning worksheet Excel must have a dedicated healthcare cost projection tab. Medicare doesn't cover everything, and a single long-term care event can wipe out decades of savings. Here's a comparison of what a basic versus advanced template actually covers:

| Feature | Basic Template | Advanced Template |

|---|---|---|

| Inflation assumption | Single flat rate (e.g., 3%) | Separate rates for medical, housing, travel |

| Withdrawal strategy | Fixed percentage every year | Variable (RMDs, Roth conversions, Social Security timing) |

| Sequence-of-returns risk | Ignored | Monte Carlo simulation or manual scenario toggles |

| Long-term care costs | Not included | Separate row with probability-adjusted cost |

Building Your Own vs. Using a Premium Template

If you're comfortable with Excel formulas, build your own from scratch. You'll understand every assumption intimately. But if you're not a spreadsheet nerd, buy a premium template from a reputable source—expect to pay $20-$50 for one that includes the features above. Avoid free downloads from random blogs; they're often broken or incomplete. The key is to customize the inflation rates for your specific location and lifestyle. If you live in a high-cost city and plan to stay, your housing inflation will differ from someone moving to rural Tennessee. Your worksheet should reflect that granularity. And for heaven's sake, include a row for "fun money." Retirement isn't just about survival—it's about living. A spreadsheet that doesn't let you budget for hobbies or travel is a spreadsheet that will make you miserable.

One Last Thing Before You Go

When you look back at the decisions that shaped your financial freedom, this quiet moment of planning right now will matter more than any market spike or sudden windfall. The numbers on your screen aren't just calculations—they're permission slips for the life you actually want to live. Whether that means retiring early, traveling more, or simply sleeping better at night, the clarity you gain from mapping out your future is the single most undervalued asset in personal finance. You don't need a perfect plan; you need a started one.

Maybe you're thinking: "I'll get to this later," or "My situation isn't complicated enough for a spreadsheet." Let me gently challenge that. The difference between people who retire comfortably and those who don't is rarely about income—it's about intention. A simple retirement planning worksheet excel file, even one with rough estimates, forces you to stop guessing and start deciding. That small friction of opening a template is the only real barrier between you and clarity. Don't let perfectionism steal your peace of mind.

Here's what I'd love for you to do next: bookmark this page so you can find it again when your financial picture shifts. Then, if you know someone who's been putting off their own retirement planning—maybe a friend, a sibling, or a colleague—share this with them. Not as a lecture, but as a lifeline. The retirement planning worksheet excel you've just learned about is a tool, but your willingness to use it is the real power. Go ahead—open the template, fill in a few cells, and see how different your future feels when you're no longer walking through fog.