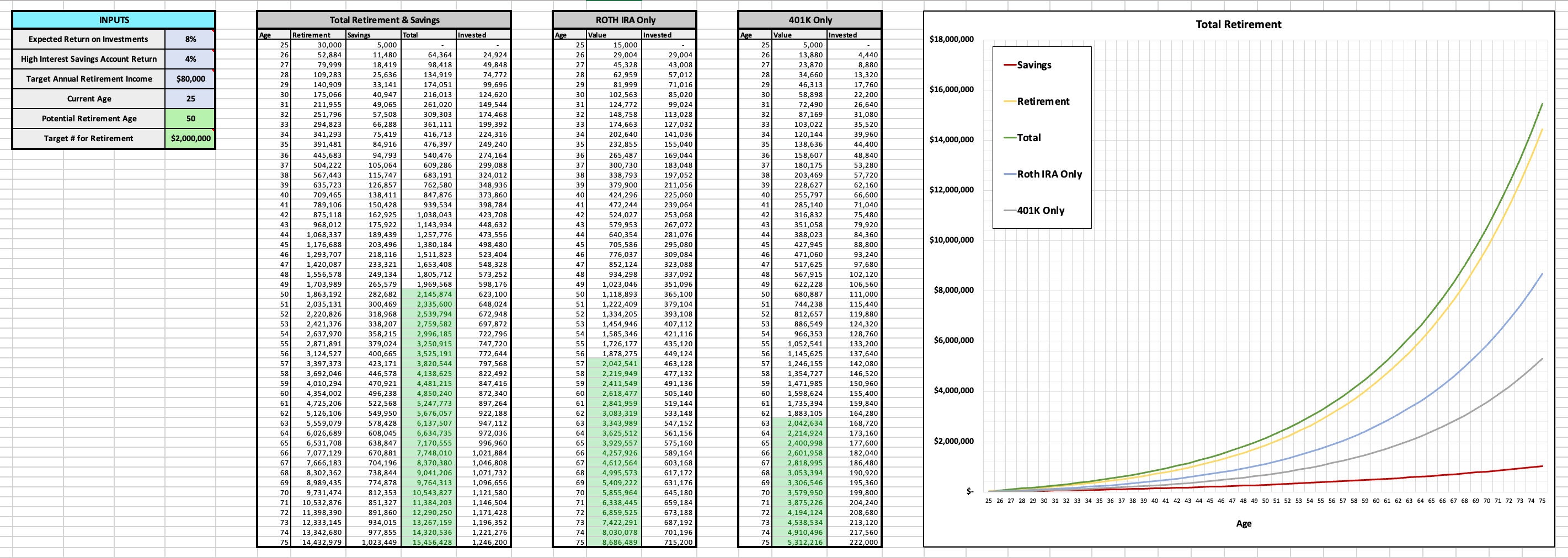

Most Indians spend decades earning money but only a few weeks actually planning where it goes after they stop working. That's a terrifying gap — and it's why most retirees end up living on far less than they expected. If you've ever stared at your bank balance wondering whether your savings will last 30 years, you already know the panic that comes with uncertainty. A retirement planning spreadsheet india isn't just a nice-to-have; it's the single tool that can stop you from guessing your future and start calculating it.

Here's the thing: inflation in India runs at 5-6% every year, medical costs are climbing at double that rate, and the average life expectancy keeps rising. Your parents' retirement math doesn't work for you anymore. Honestly, most people I talk to are shocked when they see how much they actually need — not for luxury, just for a basic dignified retirement. The spreadsheet forces you to face those numbers now, when you can still do something about them.

Look — I've seen too many smart, hardworking people realize at age 58 that their EPF and PPF combined won't cover their monthly expenses. That spreadsheet? It's your early warning system. By the time you finish reading, you'll know exactly which numbers to plug in, what assumptions most calculators get wrong, and how to build a plan that actually accounts for your real life — not some generic retirement dream. No fluff. Just the math that matters.

Why Most Retirement Calculators Miss the Real Problem in India

Let's be honest. You've probably run your numbers through a dozen online calculators, watched the little bars turn green, and felt a mild sense of accomplishment. Then reality hits. That calculator assumed a steady 8% return, zero inflation on medical costs, and that you'd somehow downsize your home in your 60s. That's where the whole exercise falls apart for most Indians. The gap between what a generic tool tells you and what actually happens when your father-in-law needs a knee replacement or your kid's wedding gets pushed up by three years is enormous. This is precisely why building your own retirement planning spreadsheet India isn't just a nerdy hobby — it's the only way to stress-test your assumptions until they break.

Here's what nobody tells you. A spreadsheet forces you to confront the uncomfortable specifics. Not "I need 2 crores." That number is meaningless. You need to know that your monthly spend at age 60 will be Rs 1.2 lakh in today's money, that your health insurance premium will double every seven years, and that you plan to gift your nephew Rs 5 lakh for his education in 2034. A generic calculator cannot handle that level of granularity. A well-built spreadsheet can, and it will show you the exact month you run out of money if you're wrong by even 1%. That's terrifying. It's also incredibly useful.

The Three Levers Nobody Wants to Pull

Most people obsess over the rate of return. They chase the perfect mutual fund, the magical small-cap bet, the "one strategy to rule them all." Meanwhile, they ignore the three levers that actually determine whether you retire broke or comfortable: your actual post-retirement withdrawal rate, the inflation assumption for healthcare specifically, and the sequence of returns risk in the first five years of retirement. If you get those three wrong, your spreadsheet is just a fancy lie. I've seen someone assume 6% inflation across the board. Medical inflation in India runs at 12-14%. That single mistake wiped out 40% of their projected corpus over a 25-year retirement.

Building a Spreadsheet That Doesn't Lie to You

Start with the absolute worst-case scenario. Assume your equity portfolio drops 30% the year you retire. Assume your rental income stops for 18 months. Assume your children need financial help longer than you planned. Then see if your numbers still work. If they do, you have a plan. If they don't, you need to adjust — either save more, retire later, or reduce your lifestyle expectations. This is the brutal honesty that a retirement planning spreadsheet India provides that no advisor will give you. Advisors want to keep you optimistic. Your spreadsheet should be a pessimist with a calculator.

| Assumption | Typical Calculator Default | Realistic India Figure |

|---|---|---|

| Inflation (general) | 6% | 7-8% |

| Medical inflation | 6% | 12-14% |

| Equity returns (post-tax) | 12% | 9-10% |

| Post-retirement withdrawal rate | 4% (US standard) | 3-3.5% (India risk premium) |

| Life expectancy assumption | 75 years | 85-90 years |

The One Actionable Tip That Changes Everything

Build a separate sheet called "Black Swan Events." List every financial disaster you can imagine — a major health crisis, a market crash that lasts five years, your child's marriage costing double your estimate. Assign a probability and a cost to each. Then run your main spreadsheet with the worst two events happening simultaneously. Yes, it's depressing. But here's the thing: once you've stress-tested your plan against the worst, the day-to-day market noise becomes background static. You stop checking your portfolio every morning. You stop panicking when the Nifty drops 5%. You just follow the plan. That peace of mind is worth more than any return you'll ever chase.

The Hidden Math of Tax and Withdrawal Sequencing

Most retirement spreadsheets treat all withdrawals as equal. They aren't. In India, the order in which you draw down your assets has a massive impact on how long your money lasts. Pull from your Provident Fund first? That's tax-free but depletes your safest bucket. Sell equity mutual funds in a down market? You lock in losses and pay capital gains tax on the gains you do have. Take money from your rental income? That's taxed at your slab rate. The sequence matters more than the total corpus in many cases. I've seen two retirees with identical Rs 3 crore portfolios end up with vastly different outcomes — one ran out at age 78, the other still had money at 85. The only difference was which account they raided first and in which market conditions.

Your retirement planning spreadsheet India needs a dedicated withdrawal strategy tab. Map out a five-year plan: Year 1-2, live off cash and fixed deposits. Year 3-5, start drawing from debt funds while equity recovers. Only after year 5 should you touch equity-heavy assets. This "bucket strategy" protects you from selling low. It's not complicated, but it requires discipline. Most people skip it because they assume they'll figure it out when the time comes. That's how you end up selling your best assets at the worst possible moment. The spreadsheet forces you to decide today, when you're calm, rather than in a panic at age 62.

One final truth: no spreadsheet can predict the future. But a good one can show you the range of possible futures — from optimistic to catastrophic. If you can survive the catastrophic one, you're ready. If your plan only works in perfect conditions, it's not a plan. It's a wish. Build the spreadsheet. Break it. Fix it. Then sleep better at night knowing you've seen the worst and prepared for it anyway.

The Part Most People Skip

You can build the most detailed retirement planning spreadsheet india has ever seen, but it won't matter if you don't let it change how you live today. This isn't about locking yourself into a future of deprivation. It's about realizing that every rupee you allocate now is a vote for the version of yourself who wakes up without an alarm, on your own schedule, with your own choices. That version of you is already in the numbers. The spreadsheet just helps you see them clearly.

Maybe a little voice is whispering, "But what if I'm too late?" Push that thought aside. The best time to start was ten years ago. The second best time is right after you finish reading this sentence. You don't need a perfect plan—you need a started one. A single contribution, a single expense trimmed, a single strategy applied today is infinitely more powerful than a perfect strategy you never begin. Your future self isn't judging you for starting late; they're grateful you started at all.

Here's your next move: bookmark this page so you can revisit the steps when motivation wavers. Better yet, share it with one person who needs to see that retirement isn't a far-off fantasy—it's a series of small, smart decisions. Then open that retirement planning spreadsheet india template you've been meaning to try, and fill in just one cell. That's all it takes to begin. Your future self is already leaning forward, waiting for you to catch up.