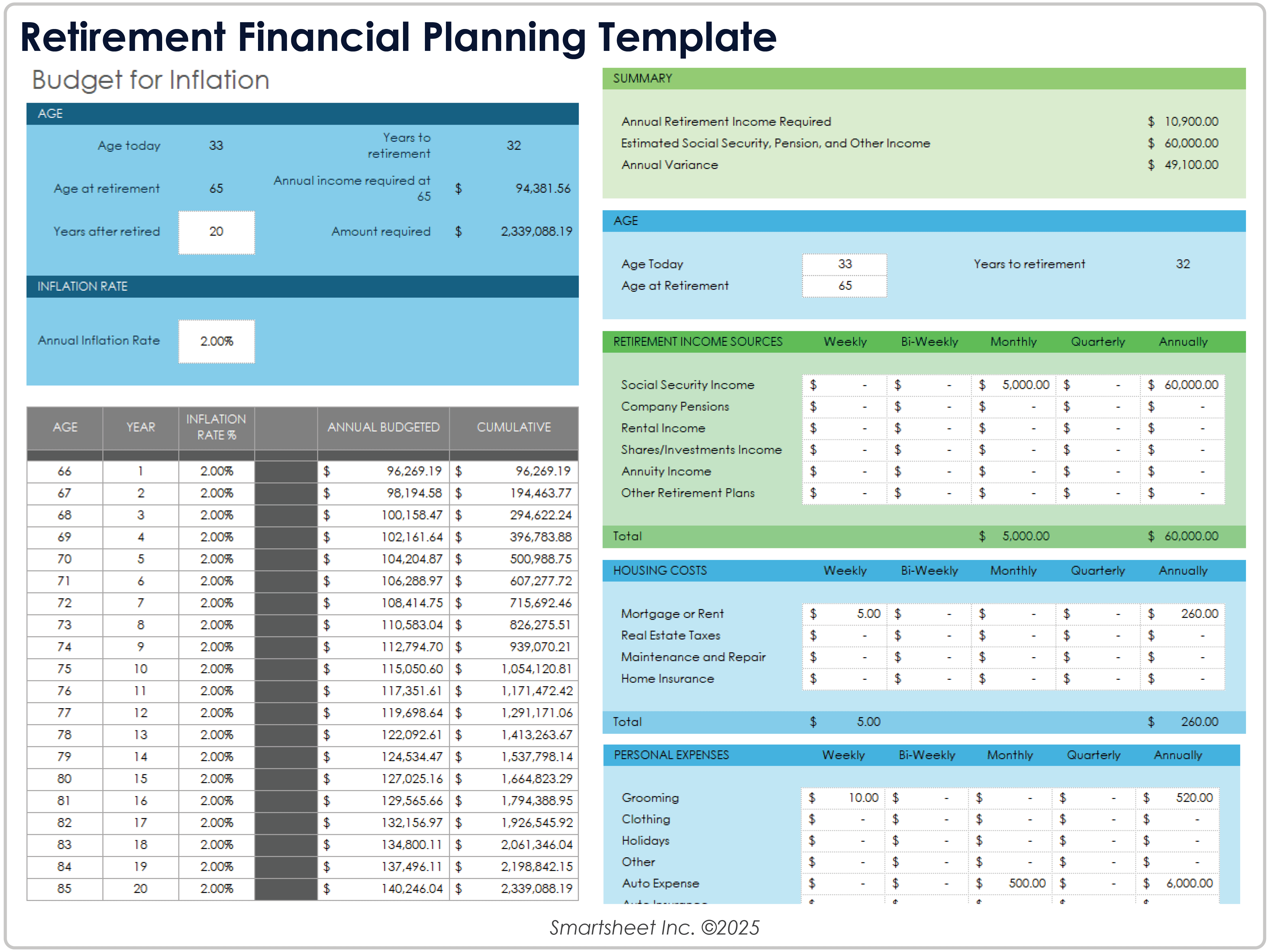

Most people are winging their retirement with a vague hope and a 401(k) balance they haven't looked at in six months. That's a recipe for waking up at 65 broke and angry. I've seen it happen to smart, hardworking people who just never bothered to run the actual numbers. Stop guessing. Get a retirement planning spreadsheet download that forces you to face the math — honestly, it's less painful than the anxiety of not knowing.

Here's the thing: inflation is still chewing through your savings, and Social Security isn't exactly a sure bet for the next generation. You need to know, right now, if you're on track to retire at 62 or if you'll be grinding until 75. Not next year. Today. This spreadsheet isn't a magic wand — it's a reality check that shows you exactly where your money is leaking or where you're actually ahead. Real talk: that feeling of "I'll figure it out later" is how people end up eating cat food in their golden years. Look — I'm not trying to scare you, just to get you to open your eyes.

What you're about to download cuts through the noise. No fluff, no motivational quotes, just hard columns for income, expenses, inflation adjustments, and withdrawal rates that actually reflect your life. You'll see the gap — or the surplus — in under ten minutes. That clarity is worth more than any investment newsletter. Keep reading to grab the exact template I use with my own family.

Why Most Retirement Spreadsheets Miss the Real Problem

Let me save you some frustration. I've been building and tweaking retirement spreadsheets for over a decade, and the biggest mistake I see people make is treating them like a simple savings calculator. You punch in your current balance, assume a 7% return, and call it a day. That's not planning. That's wishful thinking dressed up in cell borders.

The real value of a solid retirement planning spreadsheet download isn't in the numbers you input today. It's in the assumptions you force yourself to examine. Nobody tells you that the most critical column in your spreadsheet isn't your projected growth rate. It's your worst-case scenario tax drag. Most pre-built templates ignore this entirely. They assume your tax bracket stays flat for thirty years, which is laughable if you've ever watched tax policy change more than once in your lifetime.

Here's what actually works: build your spreadsheet around three distinct phases. The accumulation phase, the transition zone (those five years before retirement), and the withdrawal phase. Each one has different rules. During accumulation, you're fighting inflation and fees. During the transition, you're rebalancing asset location. During withdrawal, you're managing sequence-of-return risk. One generic growth column cannot handle all three. Yet that's exactly what 90% of free templates offer.

The Hidden Leak Most Spreadsheets Ignore

I once helped a client who had what looked like a bulletproof spreadsheet. Six percent average return, conservative spending, healthy buffer. But he'd missed something obvious: his required minimum distributions from his IRA would push him into a higher Medicare premium bracket at age 73. That cost him roughly $4,000 per year in surcharges he never modeled. A good retirement planning spreadsheet download should include a row for healthcare cost escalators and RMD triggers. If yours doesn't, you're flying blind.

What to Look For Before You Download

Before you grab the first template you find, check for three features. First, does it let you model variable withdrawal rates? The 4% rule is a starting point, not a law. Second, does it separate pre-tax, Roth, and taxable accounts? Mixing them into one "total savings" number hides the tax consequences. Third, can you run a Monte Carlo simulation or at least a simple stress test? If the spreadsheet only shows a straight line going up, it's not a plan. It's a fantasy.

| Feature | Why It Matters | Most Free Templates |

|---|---|---|

| Variable withdrawal rates | Adjusts for market downturns instead of forcing a fixed draw | Rarely included |

| Tax-bucket breakdown | Shows real after-tax income, not gross withdrawals | Often missing |

| Healthcare inflation factor | Medical costs outpace general inflation 2-3x | Almost never present |

| Social Security timing calculator | Delaying to 70 can add $100k+ in lifetime benefits | Usually a single input box |

The Real Test: Can Your Spreadsheet Survive a Bad Decade?

I run every retirement plan through a simple litmus test. I set the first ten years to negative or flat returns. No growth. Just inflation eating away at the portfolio while you're still withdrawing. If the spreadsheet still shows you solvent at age eighty-five, it's worth keeping. If it crashes to zero, you need to adjust your assumptions or your spending. This is the part most people skip because it's uncomfortable. But a retirement planning spreadsheet download that doesn't stress-test sequence-of-return risk is basically a toy.

How to Customize Without Overcomplicating

You don't need a hundred tabs. You need five: income sources, expenses, portfolio breakdown, tax projections, and a summary dashboard. That's it. I've seen people build monstrosities with conditional formatting for every scenario under the sun, and they never touch them after month one. Keep it lean. Add one new assumption per quarter. Start with inflation sensitivity. Then add longevity risk. Then add a column for one-time expenses like a new roof or a car replacement. Those lumpy costs kill more retirement plans than market crashes ever do.

One Actionable Tip That Changes Everything

Here's the specific thing nobody tells you: set a cell in your spreadsheet called "annual spending floor" and another called "annual spending ceiling." The floor is what you need to survive. The ceiling is what you want to spend in a good year. Then link your withdrawal formula to switch between them based on portfolio performance. If the market drops 15% in a year, the formula automatically drops spending to the floor. If the market gains 20%, it lifts to the ceiling. This simple toggle prevents you from selling low to fund a lifestyle you can't afford. Most retirement planning spreadsheet download templates don't include this, but you can add it in about ten minutes. Do it.

The Part Most People Skip

Here’s the truth: most people spend more time planning a two-week vacation than they do planning thirty years of retirement. That’s not a judgment—it’s just how we’re wired. The future feels abstract, while next summer’s beach trip feels real. But the quiet power of what you’ve just read is that it turns that distant, fuzzy goal into something you can touch, tweak, and track. Getting your finances right isn’t about deprivation today—it’s about buying yourself options tomorrow. What kind of options do you want when you’re sixty-five?

Maybe you’re thinking, “I’ll get to this later,” or “My situation is too messy for a simple tool.” Let me ease that hesitation right now: you don’t need a perfect plan to start—you need a starting plan that you can perfect. The messiness is exactly why a structured approach works. Every small number you plug in is a small victory over uncertainty. You don’t have to be a spreadsheet expert. You just have to be willing to begin.

So here’s your next step: bookmark this page right now, or open a new tab and grab the retirement planning spreadsheet download while it’s fresh in your mind. Better yet, send the link to one friend or family member who’s been putting this off too. That small act of sharing is how good habits spread. The retirement planning spreadsheet download won’t do the work for you—but it will make the work feel possible. And that’s the whole point.