Most Australians have no idea they're leaving tens of thousands of dollars on the table simply because they've never touched a retirement planning spreadsheet australia actually built for our tax system. Here's the thing — your super balance alone won't tell you if you're on track. I've seen couples with identical savings end up with wildly different retirement outcomes just because one of them bothered to model the numbers properly.

Right now, with cost of living chewing into savings and the super guarantee creeping up to 12%, guessing isn't an option anymore. The ATO's own data shows most retirees underestimate how much they'll actually need by about 40%. That's not a small gap — that's the difference between travelling every year and stressing about the electricity bill. You need to know exactly where you stand, not just hope for the best. Real talk: even accountants get this wrong when they eyeball it.

What I'm going to show you isn't some generic US template with dollar signs and 401(k) nonsense. It's built for Australian contributions caps, the age pension means test, and those weird little tax offsets that actually matter. You'll walk away knowing your magic number — and whether you're already past it or need to adjust course. No fluff, no motivational garbage. Just the math that actually applies to your life.

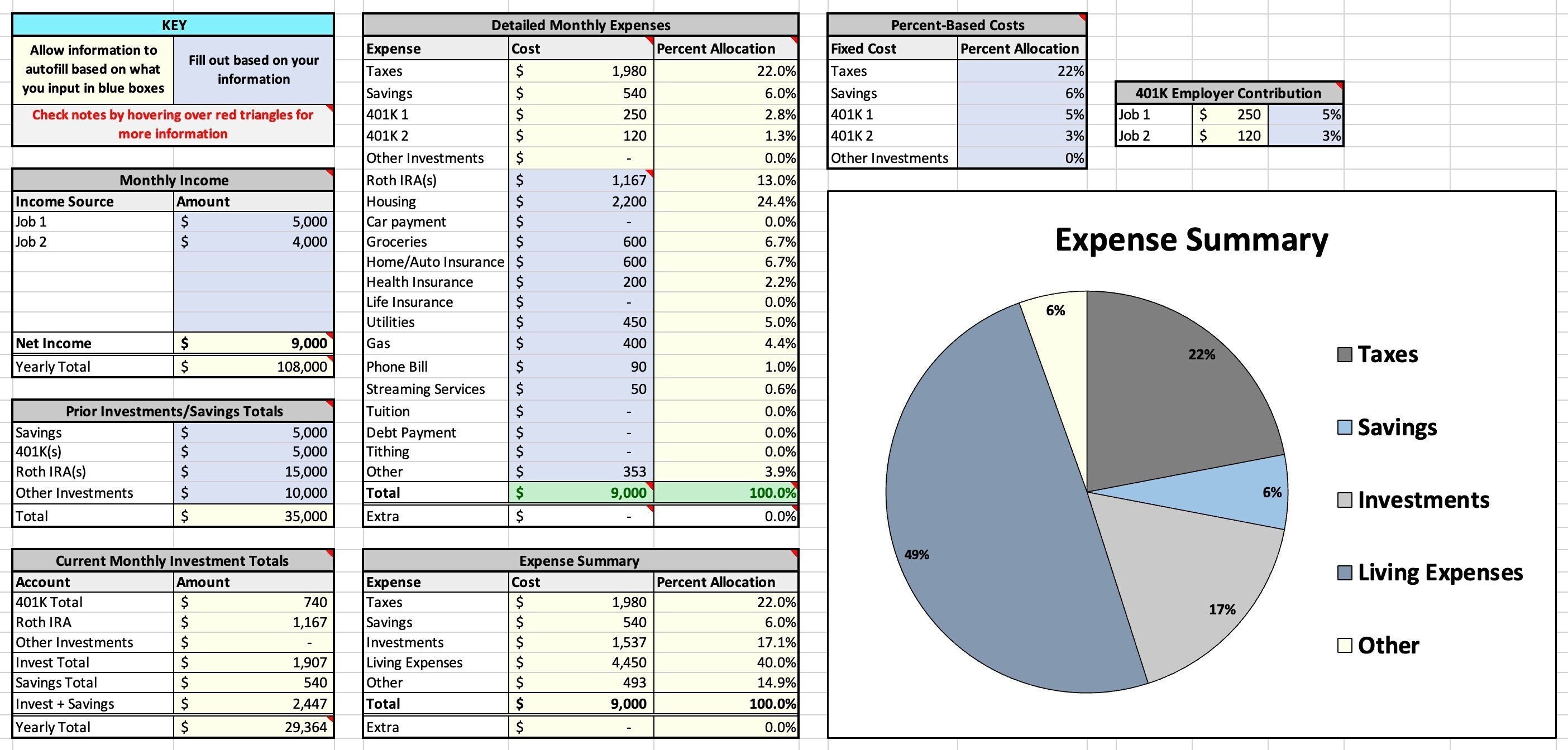

Most Australians treat retirement planning like a distant chore they'll get to eventually. They rely on the superannuation guarantee, hope for the best, and assume their savings will stretch far enough. Here's what nobody tells you: the difference between a comfortable retirement and a stressful one often comes down to a single spreadsheet that you actually update. Not a glossy app. Not a financial advisor's report you glance at once. A plain, functional spreadsheet where you track your actual spending, projected income, and the brutal reality of inflation.

The Part of Retirement Planning Most People Get Wrong

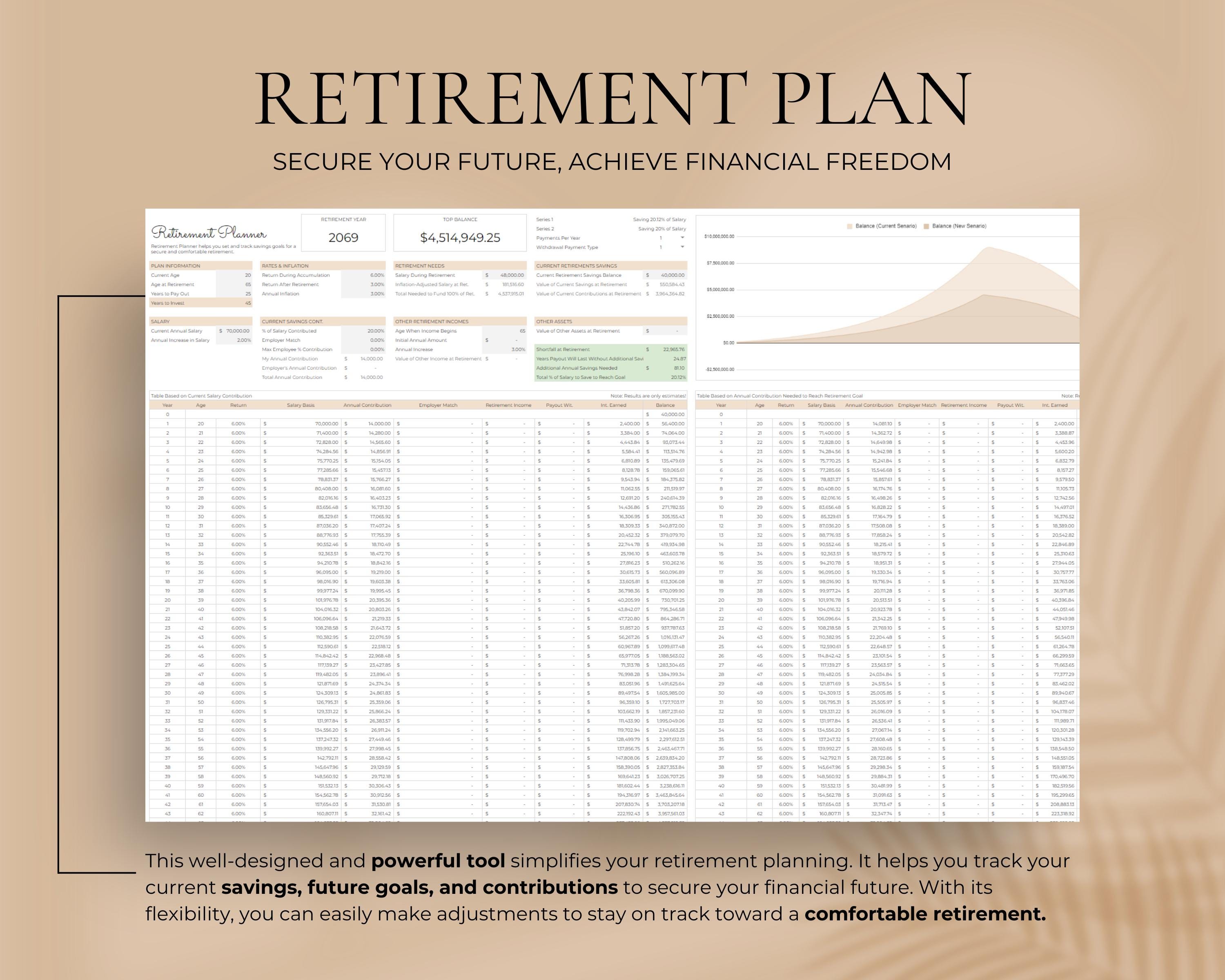

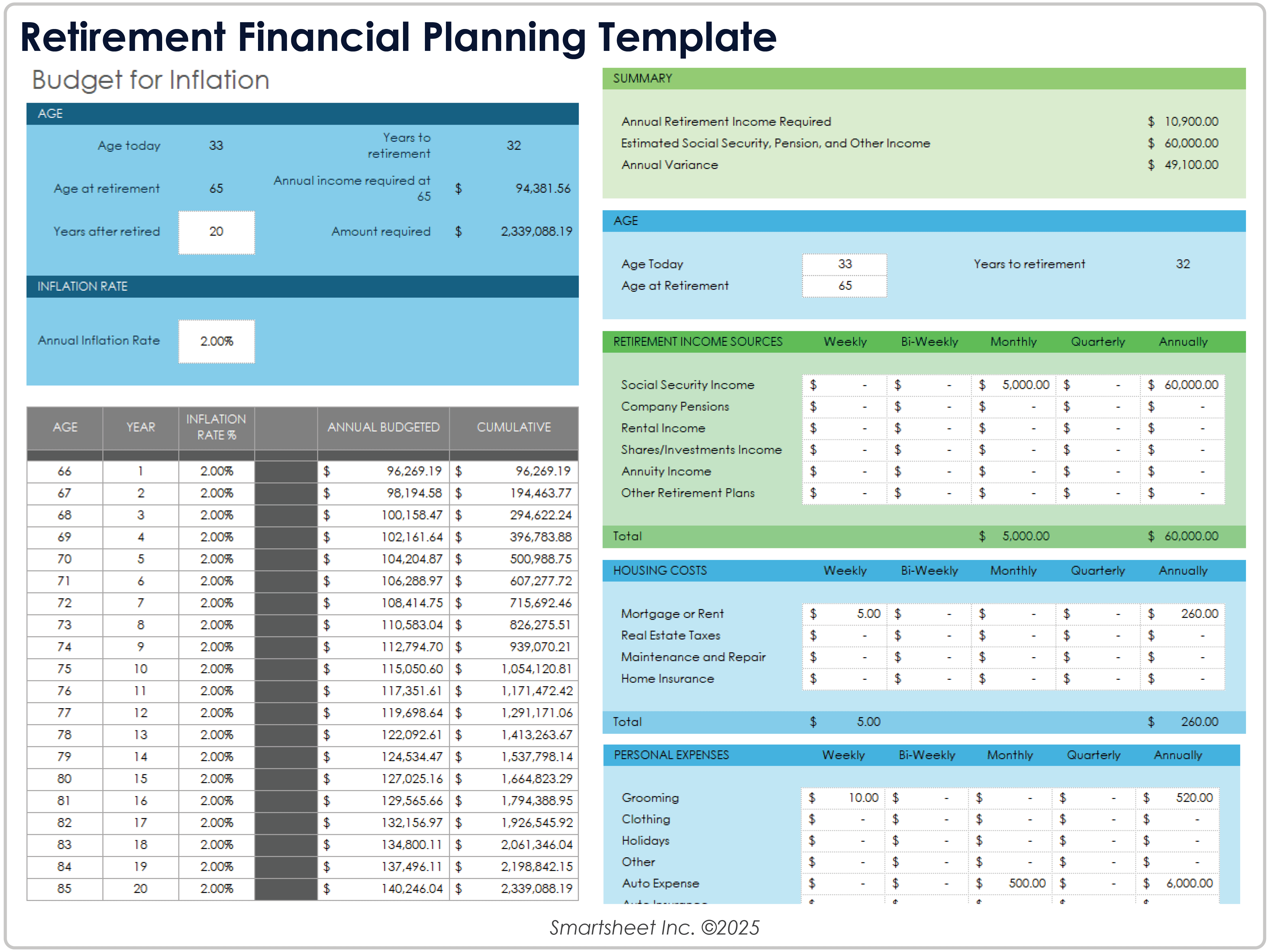

The biggest mistake I see isn't underestimating how much you need. It's overestimating how predictable your future spending will be. People plug in a flat number for living expenses and call it done. That's dangerously naive. Your spending in year one of retirement will look nothing like year ten. Healthcare costs climb. Travel enthusiasm fades. And the gap between your super balance and your actual cost of living widens faster than most calculators admit. A proper retirement planning spreadsheet Australia users swear by forces you to model these shifts. It asks uncomfortable questions: what happens if the market drops 20% in your first year? What if you live to 95? The spreadsheet doesn't judge you. It just shows you the numbers, and sometimes those numbers are sobering.

I've helped friends build these tools, and the one thing they all notice is how quickly assumptions fall apart. You think you'll spend $40,000 a year. Then you factor in replacing a car, dental work, and the occasional holiday. Suddenly you're at $55,000. And that's before you account for the aged care bond nobody wants to talk about. The spreadsheet becomes a mirror. It reflects your choices back at you without sugarcoating. That's exactly why it works.

What Your Spreadsheet Must Track Beyond the Basics

Most templates you find online stop at income versus expenses. That's table stakes. The real value lives in the variables most people ignore. You need columns for sequence-of-returns risk, which is the single biggest threat to early retirees. You need a row for home maintenance that assumes something major breaks every five years. And you absolutely must include a projection for the Age Pension means test, because the government's thresholds shift more often than you think. Here's a specific example: a client of mine assumed they'd get the full pension at 67. Their spreadsheet showed they'd actually be cut off entirely due to super assets. That saved them from a $180,000 planning error over a decade.

Building a Simple Comparison Table for Your Options

When you're deciding how to structure your retirement income, a table helps cut through the noise. Here's a realistic comparison of three common approaches you can plug into your spreadsheet:

| Strategy | Best For | Tax Impact | Risk Level |

|---|---|---|---|

| Account-Based Pension | Flexible withdrawals, growth focus | Earnings tax-free after 60 | Medium (market dependent) |

| Term Allocated Pension | Stable income, fixed timeframe | Concessional tax rates apply | Low (guaranteed payments) |

| Annuity (lifetime) | Guaranteed income, no market worry | Partial tax exemption | Very low (insurer-backed) |

Notice the risk column. Most retirees chase the middle option because it feels safe. But a lifetime annuity, while boring, protects you from outliving your money in a way no other product does. Your spreadsheet should model all three, side by side, with your actual numbers.

The One Column That Changes Everything

Add a column labelled "Buffer Events." This is where you list things like roof replacement, helping a grandchild with a house deposit, or a sudden health expense. Most Australians underestimate these by at least 40%. I've seen retirees drain their savings on a single unexpected medical bill because their spreadsheet only accounted for regular living costs. The fix is simple: add 15% to your annual expense projection as a buffer, then treat that buffer as untouchable unless an actual crisis hits. Your retirement planning spreadsheet Australia needs this line item to be realistic. Without it, you're planning for a perfect world that doesn't exist.

The Part Most People Skip

Here’s the truth that separates a comfortable retirement from a stressful one: the numbers on the page mean nothing if you don’t let them guide your decisions. You’ve just learned how to build a tool that can forecast your future, test your assumptions, and reveal blind spots you didn’t know you had. But the real power isn’t in the spreadsheet itself—it’s in the clarity it gives you to say “yes” to the right things and “no” to the distractions. This isn’t about spreadsheets; it’s about owning your timeline. What would you do differently if you knew exactly where you stood today?

I know what you might be thinking: “This looks like a lot of work, and I’m not great with formulas.” That’s okay. You don’t need to be an accountant or a data wizard. The beauty of a retirement planning spreadsheet australia is that once you set it up, it does the heavy lifting for you. Start simple—just your super balance, your age, and your target. That alone will show you more than most people ever bother to calculate. Perfection isn’t the goal; momentum is. You can always refine later.

So here’s your next step: open the spreadsheet you’ve been meaning to start, or bookmark this page so you can come back to it. Better yet, share it with one friend or family member who’s also trying to figure this out. Conversations about money get easier when you have a shared tool to look at. Let this be the moment you stop guessing and start planning. Your future self will thank you—and that’s a spreadsheet you’ll actually want to open.